(Canada Pension Plan Investment Board website)

(In 2019 Annual Report, the CPPIB claims that the fund is worth $392 billion as of March 31, 2019)

(2016, Chief Actuary claims CPP is sustainable)

(Ezra Levant of Rebel Media addresses CPP)

(Pension ponzi schemes explained)

Glowing 2016 Press Release

The press release regarding, the Chief Actuary’s report on the sustainability of the Canadian Pension Plan.

Middle class Canadians are working harder than ever, but many are worried that they won’t have enough put away for their retirement. One in four families approaching retirement—1.1 million families—are at risk of not saving enough. That is why a stronger Canada Pension Plan (CPP) is a key part of the promise that the Government of Canada made to Canadians to help the middle class and those working hard to join it.

Today, Minister of Finance Bill Morneau tabled the Chief Actuary’s 28th Actuarial Report on the CPP in Parliament. The report confirms that the contribution and benefit levels proposed under the CPP enhancement agreed upon by Canada’s governments on June 20, 2016 will be sustainable over the long term, ensuring that Canadian workers can count on an even stronger, secure CPP for years to come.

On October 6, 2016, the Government of Canada delivered on its commitment to a stronger CPP with the introduction of legislation in Parliament to implement the agreement reached by Canada’s governments to enhance the CPP to give Canadians a stronger public pension that will help them retire in dignity.

This can’t really be taken at face value, as it is all self serving. The notice fails to even acknowledge the elephant in the room, which we will get into.

Quotes From Actuary’s 2016 Report

The Canada Pension Plan Investment Board (CPPIB) invests base CPP funds according to its own investment policies which take into account the needs of contributors and beneficiaries, as well as financial market constraints. It is expected that a separate investment policy will be developed by the CPPIB with respect to the additional CPP assets. Since at the time of the preparation of the 28th Report there is no such separate investment policy in existence, the real rate of return assumption was developed to reflect the financing objective of the additional Plan. As the actual CPPIB investment strategy for the additional CPP assets becomes known, it will be reflected in subsequent actuarial reports by revising the real rate of return assumption

This is a bit troublesome. It will become “known” to the public, or it will become “known” to the people doing the investments? (Page 15 of report.)

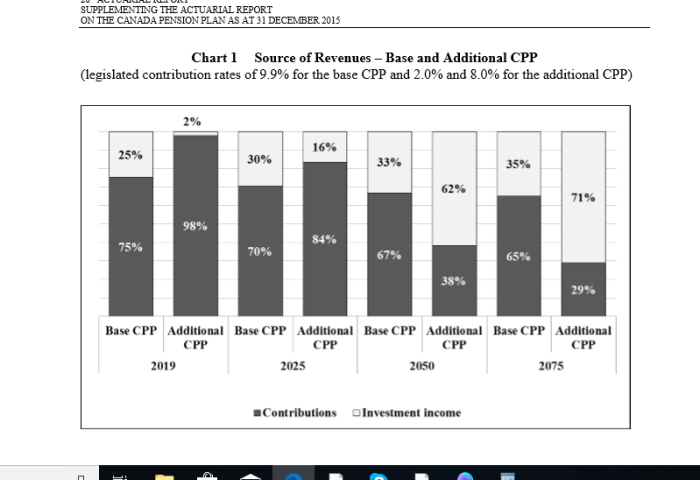

(Page 30 of report.) The CPPIB estimates that the percentage of base contributions from investment profits will creep up, and that the additional CPP will eventually become mostly funded from investment income by 2075.

The future income and outgo of the additional CPP depend on many demographic and economic factors. Thus, many assumptions in respect of the future demographic and economic outlook are required to project the financial state of the additional Plan. These assumptions impact the contribution rates, cash flows, amount of assets, as well as other indicators of the financial state. This section discusses the sensitivity of the minimum first and second additional contribution rates to the use of different assumptions than the best estimate.

Can’t fault the report for admitting it has to make assumptions. However, the trends of the current government are not great. Admitting large numbers of “refugees” who are and will remain a burden will not contribute to public coffers. Nor will vast amounts of seniors or others who won’t work. Furthermore, making industrial projects more difficult (Bills C-48 and C-69), means additional Canadians not working.

The actuarial projections of the financial state of the Canada Pension Plan presented in this report reveal that if the CPP is amended as per Part 1 of Bill C-26, the constant minimum first and second additional contribution rates that result in projected contributions and investment income that are sufficient to fully pay the projected expenditures of the additional Canada Pension Plan would be, respectively, 1.93% for the year 2023 and thereafter and 7.72% for the year 2024 and thereafter.

This report confirms that if the Canada Pension Plan is amended as per Part 1 of Bill C-26, a legislated first additional contribution rate of 2.0% for the year 2023 and thereafter, and a legislated second additional contribution rate of 8.0% for the year 2024 and thereafter, result in projected contributions and investment income that are sufficient to fully pay the projected expenditures of the additional Plan over the long term. Under these rates, assets of the additional Plan would accumulate to $70 billion by 2025, and to $1,330 billion by 2050.

No real surprise. The report concludes that the changes that the Government wants to bring in are exactly what are needed to make the plan sustainable.

CPPIB Claims Plan Sustainable Past 2090

Within this strategic framework, fiscal 2017 was a good year for CPPIB. Our diversified portfolio achieved a net return of 11.8% after all costs. Assets increased by $37.8 billion, of which $33.5 billion came from the net income generated by CPPIB from investment activities, after all costs, and $4.3 billion from net contributions to the CPP. Our 10-year real rate of return of 5.1%, after all CPPIB costs, remains above the 3.9% average rate of return that the Chief Actuary of Canada assumes in assessing the sustainability of the CPP. In his latest triennial review issued in September 2016, the Chief Actuary reported that the Base CPP is sustainable until at least 2090.

CPPIB toots its own horn, stating that the plan is sustainable at least until 2090. Page 5 is a quote from the 2017 annual report.

Quotes From 2019 CPPIB Annual Report

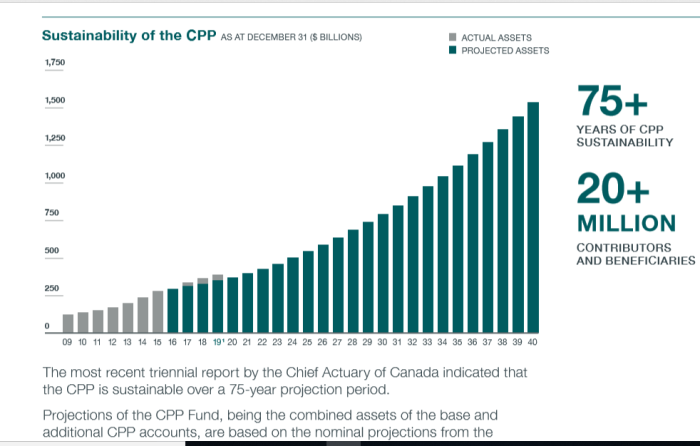

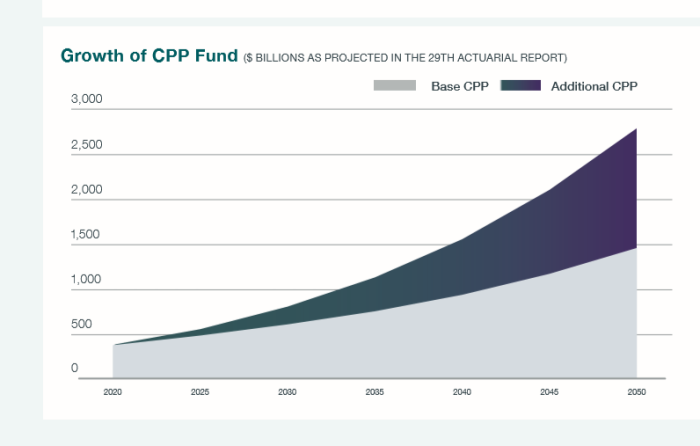

This is a graph included at the beginning of the report (page 3). It projects that by the year 2040, the Canada Pension Plan will have over $1.5 trillion in assets. This is in comparison to the $393 billion that there currently is.

It shows that actual assets have been higher than projected assets for the last 3 years.

The most recent triennial report by the Chief Actuary of Canada indicated that the CPP is sustainable over a 75-year projection period. Projections of the CPP Fund, being the combined assets of the base and additional CPP accounts, are based on the nominal projections from the 29th Actuarial Report supplementing the 27th and 28th Actuarial Reports on the Canada Pension Plan as at December 31, 2015.

The report shows a graph with projected assets. However, it doesn’t seem to address liabilities. Specifically, the pension contributions of much younger people who are paying into the system and are entitled to get it out when they retire.

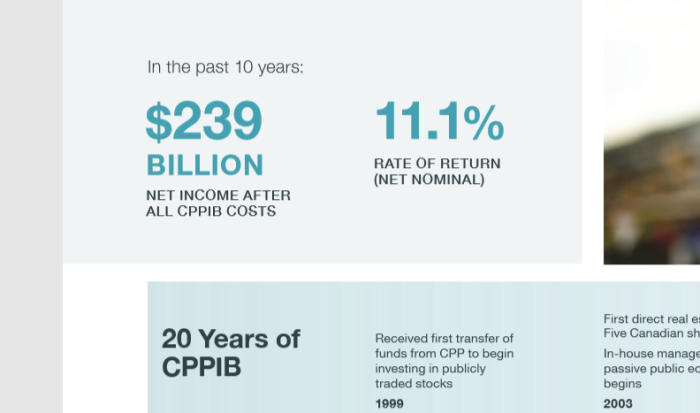

This is impressive. Over the last decade, $239 billion has been added to the fund, an equivalent of 11% annual growth. Of course, one may be forgiven for asking why premiums are so high if it’s all just going into a government fund.

CPPIB Claims Fund Is Worth Billions

Note: The sources for this data is in all of the annual reports, going back a decade, which are linked up in SECTION 1.

Inv. Income refers to investment income. This is money CPPIB claims that the funds make annually. Notice the rate of return varies from 6-18%. That is money that CPPIB makes, not money that YOU will be making from the pension plan.

| Year | Value of Fund | Inv Income | Rate of Return |

|---|---|---|---|

| 2010 | $127.6B | $22.1B | 14.9% |

| 2011 | $148.2B | $20.6B | 11.9% |

| 2012 | $161.6B | $9.9B | 6.6% |

| 2013 | $183.3B | $16.7B | 10.1% |

| 2014 | $219.1B | $30.1B | 16.5% |

| 2015 | $264.6B | $40.6B | 18.3% |

| 2016 | $278.9B | $9.1 | 6.8% |

| 2017 | $316.7B | $33.5B | 11.8% |

| 2018 | $356.B | $36.7B | 11.6% |

| 2019 | $392B | $32B | 8.9% |

The value of the pension fund is skyrocketing? Isn’t it? Looking at the values from the annual reports, it has tripled in value in just a decade. This is incredible growth.

What then is the problem?

CPPIB Has Billions In Unfunded Liabilities

Not just billions, but hundreds of billions in liabilities.

While the CPPIB staff crow about how sustainable the system is, the Office of the Superintendent of Financial Institutions had a very different conclusion.

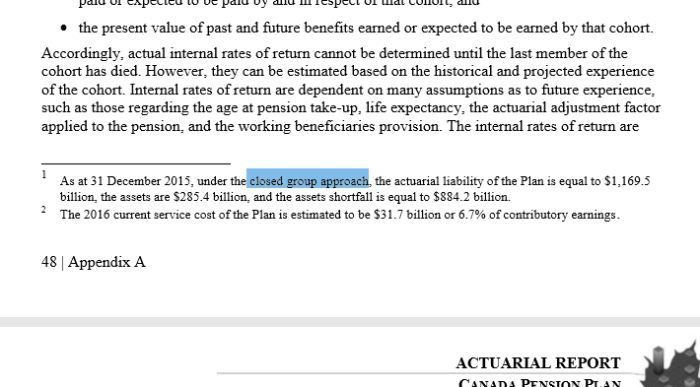

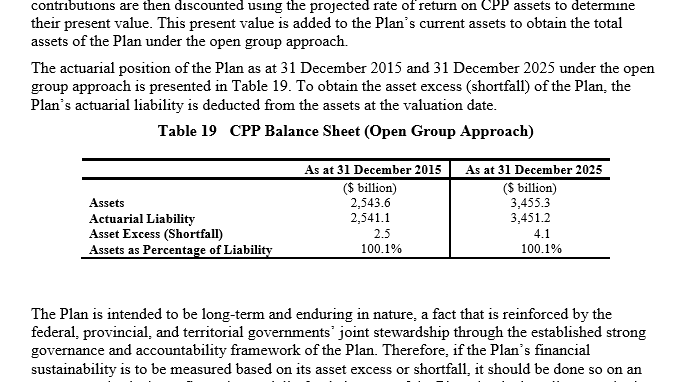

The Plan is intended to be long-term and enduring in nature, a fact that is reinforced by the federal, provincial, and territorial governments’ joint stewardship through the established strong governance and accountability framework of the Plan. Therefore, if the Plan’s financial sustainability is to be measured based on its asset excess or shortfall, it should be done so on an open group basis that reflects the partially funded nature of the Plan, that is, its reliance on both future contributions and invested assets as means of financing its future expenditures. The inclusion of future contributions and benefits with respect to both current and future participants in the assessment of the Plan’s financial state confirms that the Plan is able to meet its financial obligations over the long term1 2

What is the difference between open group basis and closed group basis?

The open group approach addresses assets and liabilities with respect to their expectations v.s. reality. The closed group approach, however, measures total assets and liabilities. And to see how much of a difference it makes, see the following two screenshots.

If you use the open group approach, everything looks fine. Reality comes very close to what you are expecting. However, the “closed group approach” takes everything into account, not just expectations.

Remember, when younger workers are paying into CPP, the organization has the money, but it isn’t theirs. It belongs to the workers, even if they won’t retire for 20, 30, or 40 years. The only way “open group approach” works is if the CPPIB had no intention of paying younger workers back.

All things considered, Canada Pension Plan is short $884.2 billion (as of 2016). This is if you don’t use selective accounting.

Paying off current obligations, by taking money from new people. Isn’t that how a ponzi scheme works? To be fair though, there is “some” investing done by CPPIB. It’s just that the bulk of the new money comes from the younger suckersworkers.

Guess this partially explains why all parties are so pro-mass-migration. Workers are needed to be shipped in to contribute deductions to fund the shortfall.

Is CPP Used To Prop Up Public Pensions?

As the federal and provincial governments continue discussing changes to the Canada Pension Plan, it is worth recalling that there are no public discussions of the most important pension issue in Canada: The unsustainable gap between the pensions of public servants and most everyone else. In fact, some critics maintain that the push to expand the CPP is driven by an unspoken need to prop up public-sector pension plans a little longer. However, doing so will only delay the inevitable overhaul of both the benefits and the funding of public-sector pensions.

The key issues surrounding public-service pension-plan benefits are mostly unspoken, both to their members and to taxpayers. Public-sector unions allow their members to believe the fiction that members contribute a fair share of their own retirement benefits, when really, the vast majority is funded by taxpayers. Few people appreciate how the CPP is folded into public-sector pension benefits: since benefits are “defined” in advance, an increase in CPP benefits reduces the amount that a public-sector pension needs to pay out to retired workers (leaving unchanged the total benefit payout to public-sector retirees). Meanwhile, taxpayers are kept in the dark about the full measure of unfunded future benefits they will have to pay, even as they shoulder more of the burden for their own retirement.

That is a theory floated over the years. Unfortunately, it gets difficult to prove given how CPPIB will not be honest about their $884.2 billion in unfunded liabilities. Their annual reports seem designed to conceal the truth.

An interesting argument though. If public sector union workers are retiring (or are retired), then they have likely been promised a good pension. However, if those union funds can’t cover it, would CPP be dipped into to make up the difference?

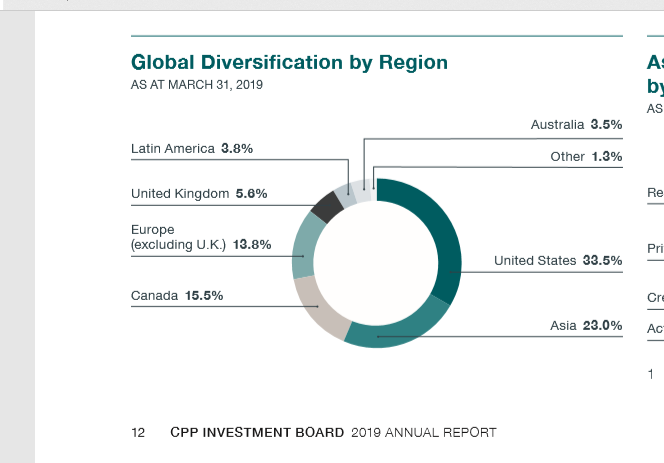

CPPIB “Invests” 85% Outside Of Canada

(From page 11 of the 2019 report)

Our 2025 strategy With two decades under our belt, CPPIB has hit its stride and truly knows its potential as a global active manager of capital. Last year, I wrote about the Board-approved strategic direction for CPPIB in 2025. Over this past year, we’ve continued to refine this 2025 strategy, and chart the course for the coming years.

Pillars of our 2025 plan include investing up to one-third of the Fund in emerging markets such as China, India and Latin America, increasing our opportunity set and pursuing the most attractive risk-adjusted returns. We have reoriented our investment departments to deliver on this growth plan, to manage a larger Fund and to achieve our desired geographic and asset diversification.

To ask the obvious question: why is the CPPIB so eager to plow its money into FOREIGN ventures? Wouldn’t putting the bulk of it into Canadian projects make more sense?

This is not just a return-on-investment issue. Plowing that money into Canadian industries would help Canadians, and help drive Canadian employment, would it not? This is supposed to be a “Canadian” pension fund.

(From page 13 of the 2019 report). The CPPIB expects that by 2050, nearly 1/2 of all income to the pension plan will be from interest and dividends on its portfolio

For reference, the fund value is calculated using this rough formula

Employee & Employer CPP Contributions + Fund Investment Returns – CPP payouts = Value

So how much of CPPIB investments are in Canada?

That’s right, just 15.5% in Canada. The other 84.5% is invested abroad. Where specifically is this money going?

(1) Midstream joint venture United States US$1.34 billion Formed a joint venture with Williams to establish midstream exposure in the U.S., with initial ownership stakes in two of Williams’ midstream systems.

(2) Grand Paris development Paris, France Formed a joint venture with CMNE, La Française’s majority shareholder, to develop real estate projects linked to the Grand Paris project, a significant infrastructure initiative in Paris.

(3) Ultimate Software United States Total value: US$11 billion Acquired a leading global provider of cloud-based human capital management solutions, alongside consortium partners Hellman & Friedman, Blackstone and GIC.

(4) CPPIB Green Bond Issuance Canada and Europe C$1.5 billion/€$1.0 billion First pension fund to issue green bonds in 10-year fixed-rate notes. Our inaugural Green Bond was a Canadian dollar-denominated bond, followed by a eurodenominated bond.

(5) ChargePoint United States Total value: US$240 million Invested as part of a funding round in preferred shares of ChargePoint, the world’s leading electric vehicle charging network.

(6) European logistics facilities Europe €450 million Formed a partnership with GLP and Quadreal to develop modern logistics facilities in Germany, France, Italy, Spain, the Netherlands and Belgium.

(7) Companhia Energética de São Paulo (CESP) São Paulo, Brazil R$1.9 billion Together with Votorantim Energia, acquired a controlling stake in CESP, a Brazilian hydro-generation company.

(8) Pacifico Sur Mexico C$314 million (initial) Signed an agreement alongside Ontario Teachers’ Pension Plan to acquire a 49% stake in a 309-kilometre toll road in Mexico from IDEAL.

(9) WestConnex Sydney, Australia Total value: A$9.26 billion Invested in WestConnex, a 33-kilometre toll road project in Sydney, alongside consortium partners Transurban, AustralianSuper and ADIA.

(10) Logistics facilities Korea Up to US$500 million Partnered with ESR to invest in modern logistics facilities in Korea.

(11) Challenger fund Australia and New Zealand A$500 million Partnered with Challenger Investment Partners to invest in middle-market real estate loans in Australia and New Zealand.

(12) Ant Financial China US$600 million Invested in Ant Financial, a company with an integrated technology platform and an ecosystem of partners to bring more secure and transparent financial services to individuals and small businesses.

(13) Renewable power assets Canada, U.S., Germany C$2.25 billion Acquired 49% of Enbridge’s interests in a portfolio of North American onshore wind and solar assets and two German offshore wind projects, and agreed to form a joint venture to pursue future European offshore wind investment opportunities.

(14) Berlin Packaging United States US$500 million Invested US$500 million in the recapitalization of Berlin Packaging L.L.C. alongside Oak Hill Capital Partners. Berlin Packaging is a leading supplier of packaging products and services to companies in multiple industries.

That’s right. Our Canadian pension fund is being used to prop up projects in: Australia, Belgium, Brazil, Germany, Italy, Mexico, the Netherlands, New Zealand, South Korea, Spain and the United States.

We won’t invest in Canadian industries, but we will bail them out. Great idea.

What about item #4, those green bonds?

CPPIB Endorses Climate Change Scam

So called green bonds are now available for sale. So state the obvious, if climate change were really a threat to humanity, then this is blatantly taking advantage of it.

Support for environmental companies or projects and clean technology is a strategic priority for EDC as demand rises for goods and services that allow for a more efficient use of the planet’s resources. Opportunities to create trade are abundant in this sector and Canada possesses a large pool of both established and emerging expertise in clean technology subsectors such as water and wastewater, biofuel, and waste to energy, to name a few.

Eligible transactions will include loans that help mitigate climate change with clean technology or improved energy efficiency. They also include transactions that specifically focus on soil, or help mitigate climate change. Our rigorous due diligence requirements ensure that all projects and transactions we support are financially, environmentally and socially responsible.

What happens when it becomes politically untenable for these globalist politicians to keep wasting taxpayer money on this hoax? Will it collapse? Will we have to perpetuate the lie in order to ensure that our “investments” don’t disappear?

Another factor that is reshaping the global investment environment is climate change. As a long-term investor, understanding environmental impacts on our investments is a key consideration and we continue to chart both the risks and opportunities stemming from climate change. This year, we launched our inaugural Green Bond, becoming the first pension fund to do so. We followed that with a euro-denominated offering. These issuances provide additional funding for CPPIB as it increases its holdings in renewables and energy-efficient buildings as world demand gradually transitions in favour of such investible assets.

(From Page 10 of the 2019 report.) Perhaps no one informed them that the climate change agenda is a scam, and has become a money pit.

This is hardly the first time that green bonds have come up. It will not be the last either.

When they say “risks and opportunities”, what are the opportunities? Will it be investing in a bubble that is sure to burst? Will it be taking advantage of desperate people?

Euro-denominated offerings? Why, is it a bigger market there?

What You Aren’t Being Told

The CPPIB admits that the bulk of its fund (around 85%) is actually invested outside of the country. That’s right, Canadians’ pension contributions being used to finance foreign investments. People assume that their money will be recirculated locally, but that is not the case.

CPPIB admits that it embraces the climate change scam. It goes as far as to endorse so-called “green bonds”. Again, this isn’t something the average person would know.

There is a credible case to be made that CPP funds are being used to top of public sector accounts, which are underfunded.

The CPP Investment Board intentionally distorts the truth about the unfunded liabilities. Using the OPEN GROUP approach, they show that actual assets are very close to expected assets, and they can cover their liabilities.

However, the more honest CLOSED GROUP approach will address “all” assets and liabilities, not just current ones. As it turns out, in 2016, the Canada Pension Plan had $285.4B in assets, and $1169.5B ($1.169.5 trillion) in liabilities. This works out to a $884.2B shortfall.

CPP is grossly underfunded.

CPP is being used to top up public pensions.

CPP is being invested in “green” schemes.

CPP is mainly being “invested” out of Canada.

CPP requires ever growing populations.

In short, we are screwed.

CPPIB AND ANNUAL REPORTS:

(1) http://www.cppib.com/en/

(2) http://www.cppib.com/documents/1800/CPPIB_F2018_Annual_Report_English.pdf

(3) http://www.cppib.com/documents/1591/2017_Annual_Report.pdf

(4) http://www.cppib.com/documents/1355/CPPIB_F2016_Annual_Report_-_ENGLISH_May_19_2016_G0UhjTk.pdf

(5) http://www.cppib.com/documents/1351/CPPIB_F2015_AR_ENG_May_21_2015_JSyvEY0.pdf

(6) http://www.cppib.com/documents/1347/CPPIB_F2014_Annual_Report_English_zZoFKwU.pdf

(7) http://www.cppib.com/documents/1339/CPPIB_Annual_Report_2013_-_English_6E8Nsli.pdf

(8) http://www.cppib.com/documents/1333/CPPIB_2012_Annual_Report_-_English_0FMf31r.pdf

(9) http://www.cppib.com/documents/1328/CPPIB_AR_2011_EN_Print_9X4nrLm.pdf

(10) http://www.cppib.com/documents/1323/CPPIB_2010_Annual_Report_English_v2_sCd3ww6.pdf

(11) http://www.cppib.com/documents/1319/CPPIB_2009_Annual_Report_English_QYpLMFZ.pdf

(12) http://www.cppib.com/en/how-we-invest/sustainable-investing/investing-reports/#/engagement

GREEN INVESTING:

(1) https://www.canada.ca/en/department-finance/news/2016/10/chief-actuary-confirms-canada-pension-plan-solid-sustainable-over-long-term.html

(2) http://www.osfi-bsif.gc.ca/Eng/Docs/cpp28.pdf

(3) https://www.edc.ca/en/investor-relations/green-bonds.html

(4) https://canucklaw.ca/international-economic-forum-of-the-americas-and-a-100t-salespitch/

(5) https://canucklaw.ca/cbc-propaganda-16-cpp-invests-2b-in-mumbai-india/

(6) https://business.financialpost.com/opinion/philip-cross-the-dirty-secret-of-a-bigger-cpp-is-that-its-to-help-bail-out-public-sector-pension-plans

(7) https://www.fraserinstitute.org/article/243000-bill-courtesy-canadas-governments

(1) http://www.osfi-bsif.gc.ca/eng/docs/cpp27.pdf (See pages 46-50)

Discover more from Canuck Law

Subscribe to get the latest posts sent to your email.