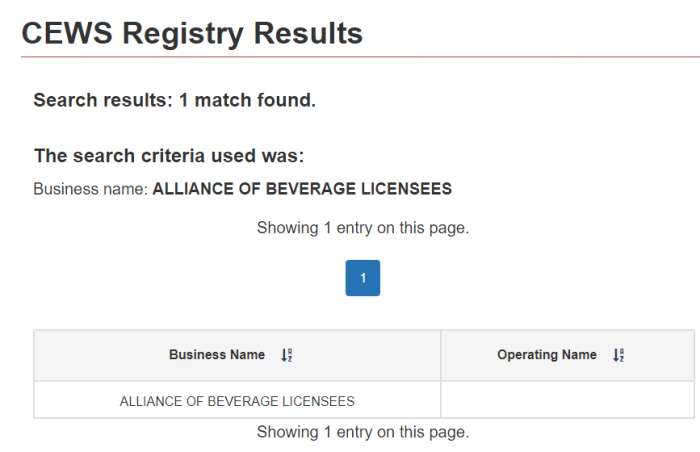

Jeff Guignard of the Alliance of Beverage Licensees B.C. claims that vaccine passports are widely supported, and that these companies “will have her [Bonnie Henry’s] back the way we have throughout the entire pandemic”. This was a July 27, 2021 showing on CTV News, and the video is posted above for full context.

This sounds lovely (or revolting) depending on your view. However, why does the Alliance of Beverage Licensees have Bonnie’s back? Why are they so supportive? Is this solidarity ideological, or financial in nature? We will get into that, and more.

At 1:07, Bonnie talks about people being more comfortable. That was basically the rationale behind masks on public transit last August. Talk about passive aggressive.

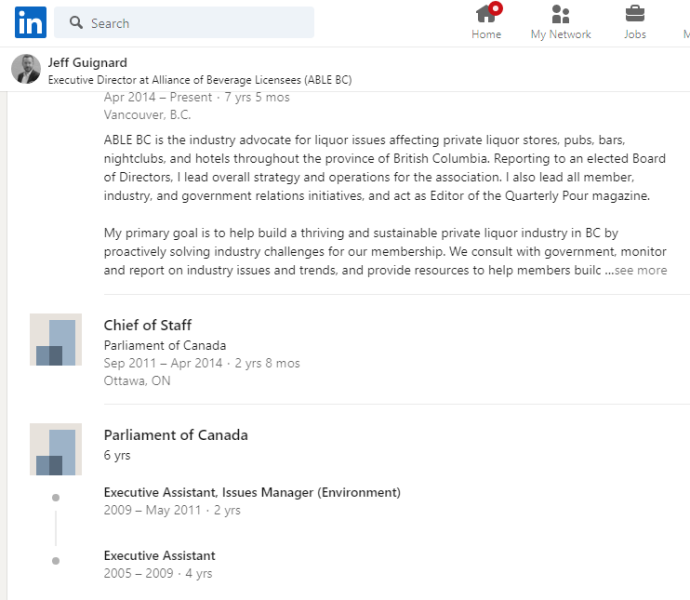

Bit of a side note: it would have been nice if in the video (see above), Guignard had disclosed the fact that he spent years as a staffer for the Liberal Party of Canada. He worked in the small business critic’s office. Of course, that same Party is now ruling Canada, and likewise supports vaccine passports. Of course, CTV didn’t take it upon themselves to mention it either, assuming they even knew about it.

Keep in mind, the British Columbia Restaurant and Foodservices Association and B.C. Hotel Association are also getting the CEWS. So are many, many organizations. Perhaps they think it unwise to bite the hand that feeds them.

As the topic of vaccine passports becomes a reality, a surprising number of retailers — across different sectors — appear to be clamouring for them. Why is that? What do they stand to gain from forcing vaccination by employees and/or customers? Won’t customers stay away, and won’t people quit? See this prior article for these passports coming to B.C.

Yes, they will quit or avoid the premises. However, given the myriad of Government programs available, it seems this is a financial decision for many. Sure, some will be driven by other things, but others see getting handouts as a worthwhile way of doing business. Free money, isn’t it?

Now, being “funded by the Government” really means being funded by the taxpayers. This happens either through direct spending, or deficit spending. Most know this of course, but it’s worth mentioning.

To be clear, this issue of taxpayers propping up businesses unnecessarily is not limited to B.C., or even to Canada. This looks like a coordinated effort to collapse economies everywhere.

A bit of a disclaimer: this is not an exhaustive list of all the grants that businesses are getting. It is, however, intended to be a guide to show just how widespread this is, and where the public’s money is really going. Also, this piece is not an authoritative source, but a good faith research effort.

To check out individual grants at the Federal level, OPEN SEARCH is a pretty good resource. The Provinces have their own listings for how they spend money.

Now, there are several programs to look at, starting with CEWS, the Canada Emergency Wage Subsidy Program. In fact, typing that into OPEN SEARCH results in thousands of hits. But in fairness, many of those were programs in place years ago, and hence irrelevant.

- Alberta Hotel & Lodging Association

- Association Des Hoteliers Du Quebec/Hotel Association of Quebec

- Association Des Hotels Du Grand Montreal

- Association Hotelier De La Region De Quebec

- British Columbia Hotel Association

- Hotel Association of Canada Inc.

- Manitoba Hotel Association Inc.

- Ottawa Gatineau Hotel Association

- Regina Hotel Association Inc.

- Saskatchewan Hotel & Hospitality Association

- The Fairways At Bear Mountain Resort Owners’ Association

- The Toronto Hotel Association

- Vancouver Hotel Destination Association

Hotel associations, as the name implies, are set up to advocate — as a bloc — for the interests of hotel owners. They subscribe to the notion of strength in numbers.

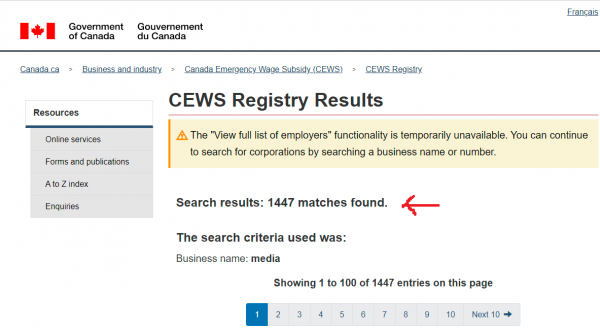

Just by typing “hotel association“, there are 13 organizations that are flagged in the CEWS program. It was set up to cover the salaries of workers, up to 75%, if they had seen a drop in income due to lockdowns and business closures.

There is currently a proposal to extend the program to October 2021. Remember, it was originally only supposed to last a few months in the Spring of 2020, to get businesses going again. Strange, that these “temporary” programs never seem to be that.

1. What is the Canada Emergency Wage Subsidy? Updated: July 2, 2021

The Canada Emergency Wage Subsidy (wage subsidy) is a subsidy that was initially available for a period of 12 weeks (made up of three four-week periods), from March 15, 2020 to June 6, 2020, that provides a subsidy of up to 75% of eligible remuneration, paid by an eligible entity (eligible employer) that qualifies, to each eligible employee – up to a maximum of $847 per week.

.

The government subsequently extended the wage subsidy until June 5, 2021, for a total of 64 weeks consisting of 16 four-week periods.

.

In the April 19, 2021 budget announcement, the government has further extended the wage subsidy for an additional 16 weeks (i.e., four more four-week periods) from June 6, 2021 to September 25, 2021, with the ability to extend the wage subsidy further to November 30, 2021

The above quote comes from the FAQ (frequently asked questions) section of the CEWS program. Talk about shifting the goalposts. Of course, this means that many businesses will be able to have wages (mostly) covered, even if they aren’t selling anything.

In fairness, the CEWS Registry doesn’t disclose how much has been paid. However, salaries are typically the single biggest expense of any company, so getting funding for that can go a long way.

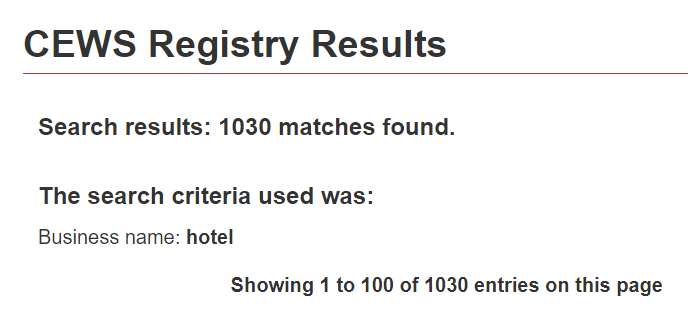

By typing in “hotel” into the CEWS search, we will see that 1030 businesses were flagged as receiving grant money. “Motel” results in another 576 hits. This does include multiples in a chain. For example, Best Western has 83 of its buildings funded with this program. Typing in “restaurant” leads to another 6065 results.

Granted, there will be a bit of overlap, but this is a good reference point.

As for all those banks, credit unions, and other financial institutions who want to vaxx their employees, start searching their names in the Registry. One can play with the CEWS search indefinitely, but we do need to move on.

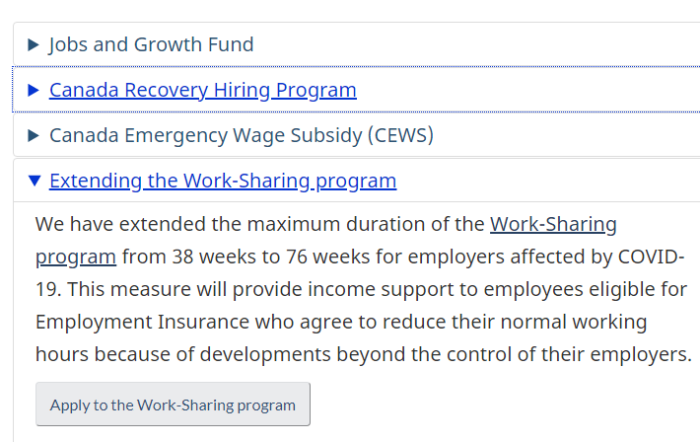

This will stand out a bit. Currently, there is the CRHP, the Canada Recovery Hiring Program. This is in some ways a substitute to the CEWS, and will subsidize the expenses of new hires. There is also the Work Sharing Program, where employees agree to work less, in order for everyone to stay employed. Think about this. Ottawa will subsidize new hires, and also pay people to work less. Or rather, the public will subsidize it.

Also, various loan and financing programs are set up to cover the gap that others will not. Guess the issue with this (one of many), is that is the loans are defaulted on, the Government could theoretically take the business. This being the same Government who caused the crash in the first place.

There are also programs to subsidize the costs of having TFW (Temporary Foreign Workers) isolated for their quarantine period. Even as we pay people to reduce their hours, or not work at all, we pay more to bring people into the country to work. Can’t make this stuff up.

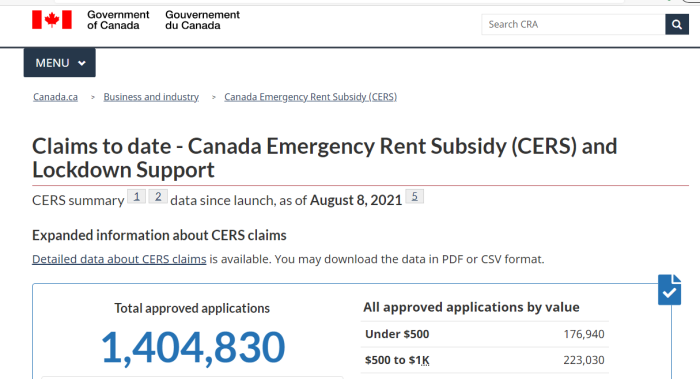

CERS, the Canada Emergency Rent Subsidy, is another major program that has become a money pit for taxpayers. Keep in mind, without the shutdowns from this fake pandemic, none of this would be needed.

The statistics page is updated regularly. As of August 8, 2021, these were 1,404,830 subsidies approved overall. Breaking it down by amounts, we get the following numbers:

| AMOUNT PAID | NUMBER OF CLAIMS |

|---|---|

| Under $500 | 176,940 |

| $500 to $1K | 223,030 |

| $1K to $1.5K | 186,140 |

| $1.5K to $2K | 146,300 |

| $2K to $4K | 333,070 |

| $4K to $10K | 230,540 |

| Over $10K | 108,800 |

That’s interesting that the numbers all seem to end in zero, but apparently that is due to rounding. There have been 1,447,690 applications received, with 203,120 unique applicants approved. This suggests that the bulk of companies are getting multiple subsidies.

As of the time of writing this, there has been $5.69 billion spent on the program, with Canada Emergency Rent Subsidy making up $4.83 billion, or the bulk, and Lockdown Support being another $859.3 million.

According to the details of the program, or each claim period, businesses can claim eligible expenses up to a maximum of:

$75,000 per business location (base and top-up)

$300,000 in total for all locations (including any amounts claimed by affiliated entities)

Keep in mind, that’s money that public is debt financing. Also, remember that many of these are in the hospitality and “non essential” sectors. This means that they have been getting paid to close, or operate on a partial capacity. These places will also be the first to implement vaccine passports.

The site also gives details on how to calculate the rent subsidy. Interestingly, the rental subsidies seem to be shrinking, while “lockdown supports” are growing.

Most people know about CERB/CRB/EI and other programs of “emergency funding”. However, it’s rather disingenuous, considering Governments are causing the crises they now claim to be preventing. The hegelian dialectic is clear for all to see.

In reality, the Governments are subsidizing companies to downsize, and people to not work. Does anyone seriously think this is about a virus?

Anyone catching on here?

The CFIB, Canadian Federation of Independent Businesses, contains a pretty thorough list of what benefits are available, both Federally and Provincially. To their credit, the coverage is quite detailed and helpful.

That said, their President, Dan Kelly, seems a bit too enthusiastic about all of this. See here and here. Some might think this whole thing is just for show. One would hope that there would be a greater emphasis on getting people back to work. There doesn’t appear to be any urgency on his part to get his members fully operational again, which is very strange.

While the CFIB may not directly be receiving money, their members pay them dues. Since this group pushes for more grants, this effectively makes the other companies middlemen.

One of the things the CFIB has been pushing for is a moratorium on evictions from commercial properties. Now, they don’t seem all that concerned with fully opening businesses up, but want them to be able to remain where they are. In essence, property rights for landlords disappears. They fight for loans, grants, and tax deferrals, but not for economic freedom.

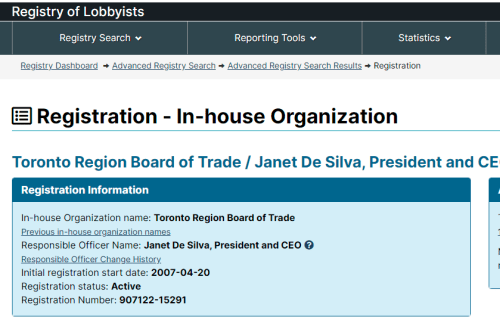

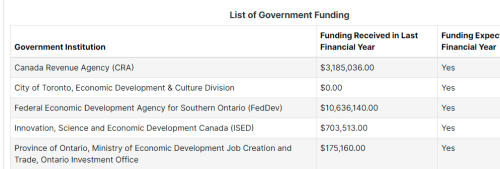

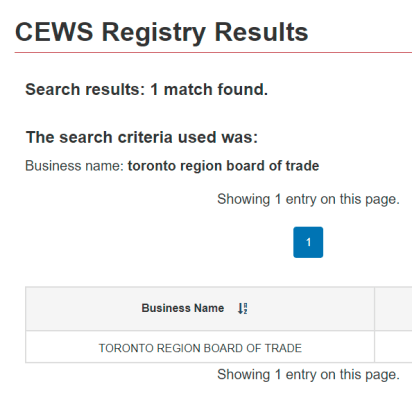

The Toronto Region Board of Trade has also loudly called for restrictions and vaccine passports. Of course, they are heavily funded by Government, and are too close with China. One would think that a group advancing “trade” would support as much freedom as possible, but it seems not. Pretty screwy when these organizations come across as more authoritarian and Communist than actual Communists.

More and more colleges and universities are demanding vaccinations. Some apply this to everyone entering the campus, while others limit it to those living in dormitories. Oddly, they never mention that these injections are still only authorized on an interim basis, and not formally approved. Most are actually registered charities, whose finances are propped up under this classification.

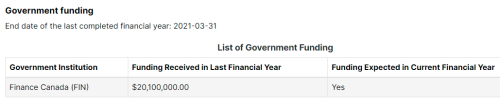

Chapters-Indigo became notorious for not allowing people in without masks, even those with legitimate medical exemptions. Of course, Canadians propped this company up with over $20 million in handouts in the year 2020. Sure, we can boycott them, but it’s pretty meaningless when they just get bailed out. While they haven’t announced a vaccine passport requirement (yet), this company seems pretty likely to.

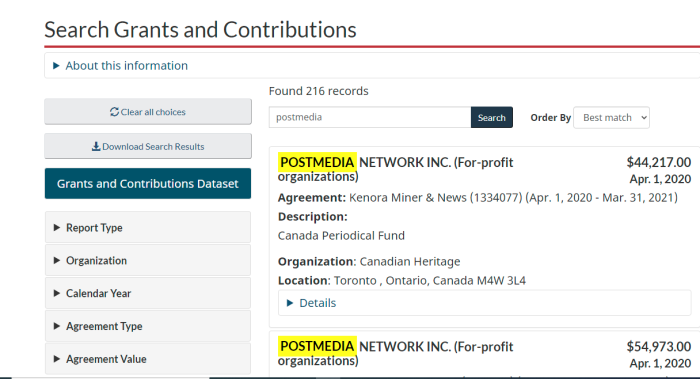

Of course, the media in Canada cheers loudly for more restrictions, more lockdowns, and more erosion of basic rights. Even “alternative” media and journalists offer only the most tepid opposition. Of course, looking at some of the grants they get (see bottom of article), things start to make sense. Additionally, this doesn’t include all of the ad space that gets bought up by Federal and Provincial Governments. Heck, the whole series is worth checking out.

| GROUP | YEAR | AMOUNT |

|---|---|---|

| Agence Science-Presse | 2019-2020 | $129,345 |

| Apathy is Boring | 2018-2019 | $100,000 |

| Apathy is Boring | 2019-2020 | $340,000 |

| Boys and Girls Clubs of Canada | 2019-2020 | $460,000 |

| Canadian News Media Association | 2019-2020 | $484,300 |

| CIVIX | 2018-2019 | $275,000 |

| CIVIX | 2019-2020 | $400,000 |

| Encounters with Canada | 2018-2019 | $100,000 |

| Quebec Professional Journalists | 2019-2020 | $202,570 |

| Global Vision | 2019-2020 | $260,000 |

| Historica Canada | 2019-2020 | $250,000 |

| Institute for Canadian Citizenship | 2019-2020 | $250,000 |

| Journalists for Human Rights | 2019-2020 | $250,691 |

| Magazines Canada | 2019-2020 | $63,000 |

| McGill University | 2019-2020 | $1,196,205 |

| MediaSmarts | 2019-2020 | $650,000 |

| New Canadian Media | 2019-2020 | $66,517 |

| Ryerson University | 2019-2020 | $290,250 |

| Samara Centre for Democracy | 2019-2020 | $59,200 |

| Sask Weekly Newspapers Ass’n | 2019-2020 | $70,055 |

| Simon Fraser University | 2019-2020 | $175,000 |

| Vubble Inc. Unboxed project | 2019-2020 | $299,000 |

As just a very small sample, these are some of the “anti-misinformation” grants that had been handed out. Note: this is prior to the so-called pandemic, and mostly center around elections and democracy. It speaks volumes when not only is the media Government funded, but the fact checkers are as well.

And this doesn’t even cover the social media collusions, and censorship. They don’t even bother to hide that anymore.

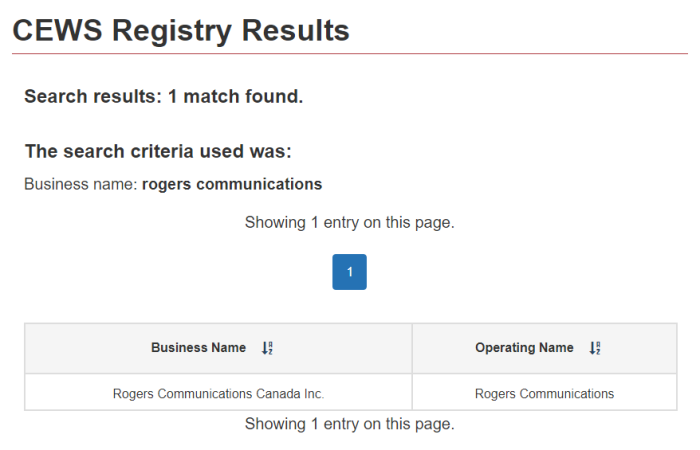

Have you also noticed how more and more sports teams are demanding vaccinations from both players and fans? Take a look through the CEWS index. A surprising number of them are getting the wage subsidy. Imagine this: your taxes pay for this (now even more so), and in order to attend a game, you need to have a vaccine and a mask, and shell out outrageous amounts to millionaire athletes.

One such example is the Toronto Blue Jays, which is owned by Rogers Communications. They just made the announcement that everyone — including fans — would either need a vaccine passport, or a negative test. This is, of course, just one of many who are being funded by the public, to exclude the public.

Do you get it now, Canadians? Can you see why there are so many people that would be happy to keep the scam-demic going? There’s a lot of money to be made in all of this, including by crashing the economy. Experts like Abdu Sharkawy do quite well on the speaking circuit, spreading doomsday warnings.

This only ends in one of two ways: either society collapses, or there is sufficient pushback to stop it. At this point, option #1 seems more likely.

IMPORTANT LINKS

(1) https://bc.ctvnews.ca/not-vaccinated-against-covid-19-b-c-s-health-officials-say-there-will-be-consequences-1.5525139

(2) https://www.linkedin.com/in/jeff-guignard-62020a32/

(3) https://lobbycanada.gc.ca/app/secure/ocl/lrs/do/cmmLgPblcVw?comlogId=245488

(4) https://search.open.canada.ca/en/gc/

(5) https://canucklaw.ca/b-c-mandates-vaccine-passports-no-emergency-order-no-approval-no-exemptions-audio/

(6) https://apps.cra-arc.gc.ca/ebci/hacc/cews/srch/pub/bscSrch

(7) https://www.canada.ca/en/revenue-agency/services/subsidy/emergency-wage-subsidy.html

(8) https://archive.is/7imOj

(9) https://www.canada.ca/en/revenue-agency/services/subsidy/emergency-wage-subsidy/cews-frequently-asked-questions.html

(10) https://archive.is/51VAH

(11) https://www.canada.ca/en/department-finance/economic-response-plan.html

(12) https://archive.is/osD91

(13) https://www.canada.ca/en/revenue-agency/services/subsidy/emergency-rent-subsidy.html

(14) https://archive.is/Lz8LI

(15) https://www.canada.ca/en/revenue-agency/services/subsidy/emergency-rent-subsidy/cers-statistics.html

(16) https://www.canada.ca/en/revenue-agency/services/subsidy/emergency-rent-subsidy/cers-calculate-subsidy-amount.html

(17) https://twitter.com/CFIB/status/1402405151483248645

(18) https://twitter.com/CFIB/status/1395133016423505923

(19) https://lobbycanada.gc.ca/app/secure/ocl/lrs/do/vwRg?cno=15291®Id=911677

(20) https://lobbycanada.gc.ca/app/secure/ocl/lrs/do/vwRg?cno=369554®Id=913010

(21) https://www.cbc.ca/news/canada/london/her-daughter-has-a-mask-exemption-but-chapters-indigo-wouldn-t-let-her-in-1.5942044

(22) https://www.cp24.com/news/toronto-blue-jays-to-mandate-covid-19-vaccines-or-negative-tests-for-everyone-12-and-up-starting-sept-13-1.5557603

(23) https://www.nsb.com/speakers/abdu-sharkawy/

MEDIA SUBSIDIZED BY TAXPAYERS

(A) https://canucklaw.ca/postmedia-subsidies-connections-may-explain-lack-of-interest-in-real-journalism/

(B) https://canucklaw.ca/postmedia-gets-next-round-of-pandemic-bucks-from-taxpayers-in-2021/

(C) https://canucklaw.ca/nordstar-capital-torstar-corp-metroland-media-group-more-subsidies-pandemic-bucks/

(D) https://canucklaw.ca/aberdeen-publishing-sells-out-takes-those-pandemic-bucks-to-push-narrative/

(E) https://canucklaw.ca/many-other-periodicals-receiving-the-pandemic-bucks-in-order-to-push-the-narrative/

(F) https://canucklaw.ca/media-subsidies-to-counter-online-misinformation-groups-led-by-political-operatives/

(G) https://canucklaw.ca/taxpayer-grants-to-fight-misinformation-in-media-including-more-pandemic-bucks/

(H) https://canucklaw.ca/counter-intelligence-firms-to-influence-elections-canada-and-abroad-registered-as-charities/

(I) https://canucklaw.ca/more-pandemic-bucks-for-disinformation-prevention-locally-and-abroad-civix/

(J) https://canucklaw.ca/phac-supporting-science-up-first-online-counter-misinformation-group/

(K) https://canucklaw.ca/even-more-subsidies-pandemic-bucks-for-propping-up-canadian-media/

(L) https://canucklaw.ca/sister-of-pro-lockdown-mayor-john-tory-a-board-member-at-bell-which-received-cews-tax-breaks/

(M) https://canucklaw.ca/disinfowatch-ties-to-atlas-network-connected-to-lpc-political-operatives/