BIS, the Bank for International Settlements, is working towards implementing a digital currency that would replace cash. There doesn’t appear to be any ideological concerns against this. Instead, it becomes a matter of details.

1. BIS Working Our Details Of Digital Currency

Yet the world is changing. Even before Covid-19, cash use in payments was declining in some advanced economies. Commercially provided, fast and convenient digital payments have grown enormously in volume and diversity. To evolve and pursue their public policy objectives in a digital world, central banks are actively researching the pros and cons of offering a digital currency to the public (a “general purpose” central bank digital currency (CBDC)). Understanding of CBDCs has advanced significantly in the last few years. Published research, policy work and proofs-of-concept from central banks have gone a long way towards establishing the potential benefits and risks.

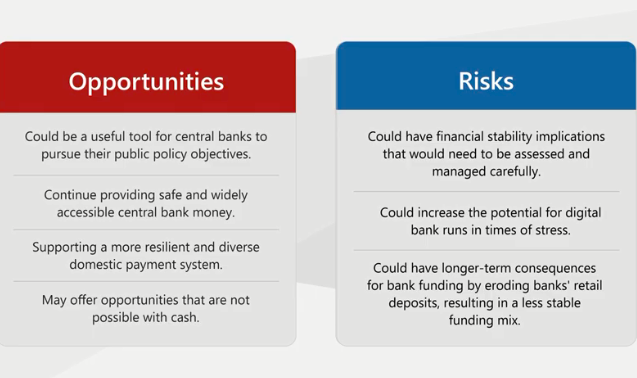

For the central banks contributing to this report, the common motivation for exploring a general purpose CBDC is its use as a means of payment. Providing cash to the public is a core responsibility of central banks and a public good. All the contributing central banks commit to continue providing cash as long as there is public demand. Yet a CBDC could provide a complementary central bank money to the public, supporting a more resilient and diverse domestic payment system. It might also offer opportunities not possible with cash while supporting innovation.

2.1 Payment motivations and challenges

2.1.1 Continued access to central bank money

In jurisdictions where access to cash is in decline, there is a danger that households and businesses will no longer have access to risk-free central bank money. Some central banks consider it an obligation to provide public access and that this access could be crucial for confidence in a currency. A CBDC could act like a “digital banknote” and could fulfil this obligation.

2.1.2 Resilience

Cash serves as a backup payment method to electronic systems if those networks cease to function. However, if access to cash is marginalised, it will be less useful as a backup method if the need arises. A CBDC system could act as an additional payment method, improving operational resilience. Compared to cash, a CBDC system might provide a better means to distribute and use funds in geographically remote locations or during natural disasters.

However, significant offline capabilities would need to be developed, both for the CBDC system and any dependencies (eg some availability of electricity for mobile devices). Counterfeiting and cyber risk present a challenge. Cash has sophisticated anti-counterfeiting features and large-scale issues rarely occur. Theoretically, a successful cyber attack on a digital CBDC system could quickly threaten a significant number of users and their confidence in the wider system (as it could for a large bank or payment service provider). Defending against cyber attacks will be made more difficult as the number of endpoints in a general purpose CBDC system will be significantly larger than those of current wholesale central bank systems.

References

- Adrian, T and T Mancini Griffoli (2019): “The rise of digital money”, IMF FinTech Notes, no 19/001, July.

- Auer, R and R Böhme (2020): “The technology of retail central bank digital currency”, BIS Quarterly Review,

March, pp 85–100. - Auer, R, G Cornelli and J Frost (2020): Rise of the central bank digital currencies: drivers, approaches and

technologies”, BIS Working Papers, no 880, August. - Auer, R, P Haene and H Holden (2020): Multi CBDC arrangements and the future of cross-border payments,

BIS papers, forthcoming. - Bank of Canada (2020): Contingency planning for a central bank digital currency, February.

- Bank of Canada and Monetary Authority of Singapore (2019): Enabling cross-border high value transfer

using distributed ledger technologies, May. - Bank of England (2020): Central bank digital currency: opportunities, challenges and design, March.

- Bank of Thailand and Hong Kong Monetary Authority (2020): Inthanon-LionRock: leveraging distributed

ledger technology to increase efficiency in cross-border payments, January. - Bech, M and R Garratt (2017): “Central bank cryptocurrencies”, BIS Quarterly Review, September, pp 55–

70. - Bindseil, U (2020): “Tiered CBDC and the financial system”, ECB Working Paper Series, no 2351, January.

- Boar, C, H Holden and A Wadsworth (2020): “Impending arrival – a sequel to the survey on central bank

digital currency”, BIS Papers, no 107, January. - Bossone, B (2001): “Should banks be narrowed?”, IMF Working Papers, WP/01/159, October.

- Brunnermeier, M, H James and J-P Landau (2019): “The digitalization of money”, NBER Working Papers, no

26300, September. - Committee on Payments and Market Infrastructures (2018): Cross-border retail payments, February.

——— (2020): Enhancing cross-border payments: building blocks of a global roadmap, July. - Committee on Payments and Market Infrastructures and Markets Committee (2018): Central bank digital

currencies, March. - Committee on Payments and Market Infrastructures and World Bank Group (2020): Payment aspects of

financial inclusion in the fintech era, April. - Committee on Payment and Settlement Systems (2003): The role of central bank money in payment

systems, August. - European Central Bank and Bank of Japan (2019): Synchronised cross-border payments, June.

- European Central Bank and Bank of Japan (2020): Balancing confidentiality and auditability in a distributed

ledger environment, February. - Ferrari, M, A Mehl and L Stracca (2020): Central bank digital currency in the open economy, forthcoming.

G7 Working Group on Stablecoins (2019): Investigating the impact of global stablecoins, October. - Kahn, C, F Rivadeneyra and R Wong (2018): “Should the central bank issue e-money?”, Bank of Canada Staff Working Paper, 2018-58, December.

- Sveriges Riksbank (2018): The Riksbank’s e-krona project, report 2, October

This goes far beyond some academic theory. There has been serious research and study into issuing digital currency, and it has gone on for quite some time. The “pandemic” seems to be a pretext to push it further along.

Nice to see that some of the major risks are addressed, such as hacking, or system malfunction erasing financial information.

Also, this must be pointed out: most central banks are privately owned and/or controlled. This means that countries must borrow (at interest) in order to get money for day to day operations. Such a system is not necessary, but is enacted for the purposes of creating endless debt slavery. Politicians go along with this because they have no interest in the well being of their people.

2. The Fraud Of Private Central Banking

One of the reasons that digital currency is touted is supposedly to combat money laundering. Interesting, because private central banking (money borrowed at interest), is arguably the greatest financial fraud ever perpetuated. In this scheme, the only way countries can get money — created from nothing — is to borrow it at interest.

3. Digital Currency Openly Discussed

This discussion is hardly limited to BIS. Banks and financial institutions across the planet are talking about how to implement such a system, and have been doing so for many years.

A curious point: things like Bitcoin are promoted as a decentralized way to make transactions, yet banks talk about ways to centrally manage these.

4. Bank For Int’l Settlements Innovation Hub

Hub projects and topics will evolve over time, and the BIS has been working to identify areas of work for the Hub that reflect the innovation priorities of the central bank community and which could be scaled up through international cooperation. Topics under consideration for the work agenda include central bank digital currencies, global stablecoins, payment innovations, the impact of big tech on financial intermediation, regtech and suptech, fast-paced electronic markets, and digitalisation of trade finance.

What does the BIS Innovation Hub do?

The mandate of the BIS Innovation Hub is to identify and develop in-depth insights into critical trends in financial technology of relevance to central banks, to explore the development of public goods to enhance the functioning of the global financial system, and to serve as a focal point for a network of central bank experts on innovation. It complements the already well established cooperation within the BIS-hosted committees.

Digital currency is just one of the things that BIS is working on. The group wants to be at the forefront of the trends that are emerging in financing and payment processing.

5. Privacy Element Missing From Discussion

What about people who want to make business transactions without there being a record for many years? Not everyone is okay with every food or minor purchase being a record available for others to see. Although a growing population seems unconcerned with such things, there is the inherent loss of privacy.

And what about the loss of anonymity or choice when it comes to association, or viewpoints? Is it not easier to connect a person (and their public statements), to their finances? If they happen to hold “incorrect” views, what’s to stop there digital currency from being erased? What’s to prevent institutions from refusing to do business with them? For a concrete example, banks these days are promoting forced diversity and globalism, although many are opposed to it.

Although this sounds farfetched, what’s to stop a Chinese style “social credit” system from making someone’s life impossible to live? Such a thing is possible then finance and identity cannot be separated.

https://www.bis.org/press/p201009.htm

https://www.bis.org/publ/othp33.pdf

BIS Digital Currency Paper

BIS Video Promoting Digital Currency

Citi On Digital Currency (Video)

Digital Currency Discussion, India(Video)

Various Digital Currency Options

World Affairs Council On Digital Currency (Video)

Bank For International Settlements Innovation Hub

BIS on digital innovation options