(This “charity” was originally called the Independent Immigration Aid Association. The goal was to help settle British immigrants into BC. It was acquired by Malcolm, renamed, and used for tax purposes for her media company.)

(From later in 2020. Interesting that a group claiming to provide independent coverage of the Government is in fact receiving subsidies from the same Government, to keep its operations going)

1. Media Bias, Lies, Omissions And Corruption

(1) https://canucklaw.ca/media-1-unifor-denies-crawling-into-bed-with-government

(2) https://canucklaw.ca/full-scale-of-inadmissibles-getting-residency-permits-what-global-news-leaves-out/

(3) https://canucklaw.ca/media-3-post-media-controls-msm-conservative-alternative-media/

(4) https://canucklaw.ca/media-4-much-conservative-content-dominated-by-koch-atlas/

2. Important Links

(1) https://tnc.news/about-us/

(2) http://archive.is/fOUxQ

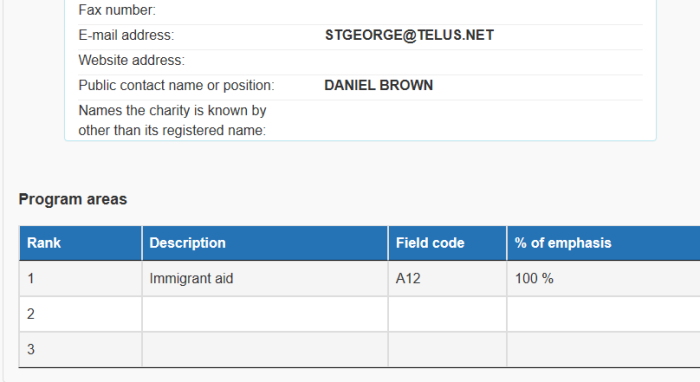

(3) information about TNC on CRA website,

(4) http://archive.is/0Yquf

(5) 2015 Registered charity information return

(6) https://www.atlasnetwork.org/news/article/42-free-market-leaders-complete-think-tank-leadership-training

(7) http://archive.is/Y5fGh

(8) https://www.theglobeandmail.com/news/politics/kenneys-office-apologizes-for-new-canadians-stunt-on-sun-news/article543280/

(9) http://archive.is/Mwsba

(10) https://policyoptions.irpp.org/2016/07/06/a-response-to-candice-malcolms-losing-true-north/

(11) http://archive.is/N0j3Q

(12) https://www.cbc.ca/news/politics/fired-kenney-staffer-makes-a-comeback-1.1075263

(13) http://archive.is/rat87

(14) https://www.can1business.com/company/Active/Independent-Immigration-Aid-Association

(15) http://archive.is/3u4kU

(16) https://decisions.fct-cf.gc.ca/fc-cf/decisions/en/item/424449/index.do

(17) http://archive.is/FYtSb

(18) https://apps.cra-arc.gc.ca/ebci/hacc/srch/pub/dsplyBscSrch

3. Previously Covered By Press Progress

CLICK HERE, for prior coverage by PressProgress.ca.

When researching into True North Center’s tax returns and history, I stumbled across this piece on the subject. Quite thorough, and difficult to add to this, but let’s try anyway.

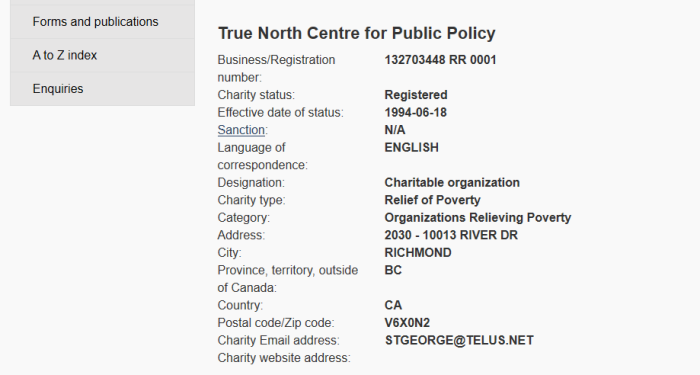

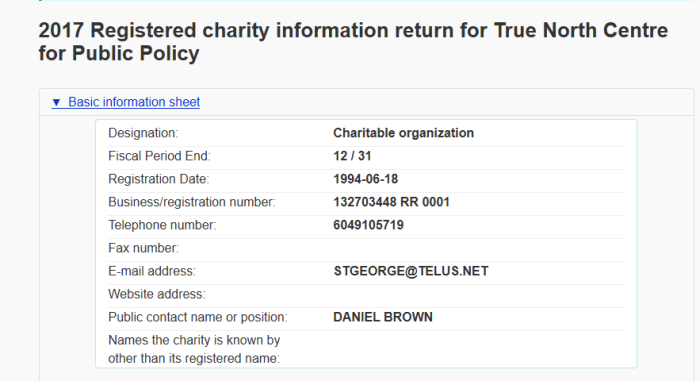

4. True North Originally Called I.I.A.A.

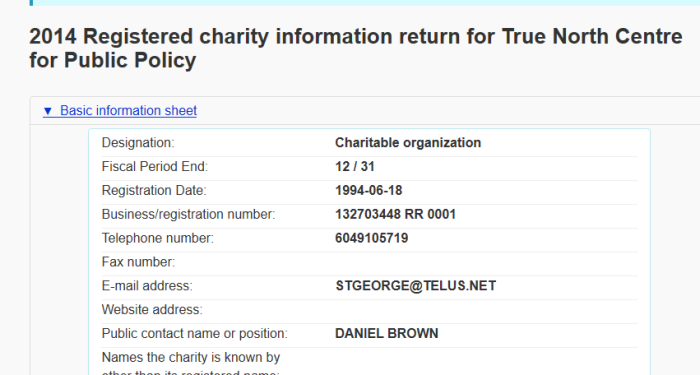

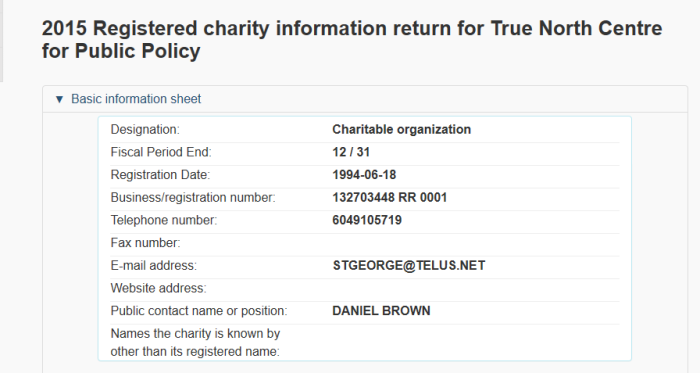

From Data On CRA Website

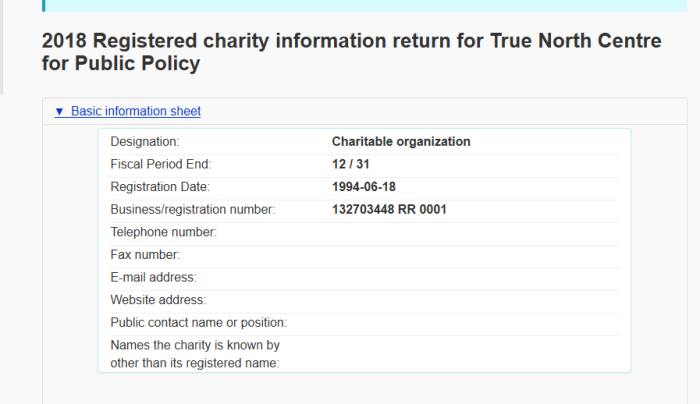

True North Centre for Public Policy

Business/Registration number: 132703448 RR 0001

Charity status: Registered

Effective date of status: 1994-06-18

Designation: Charitable organization

Charity type: Relief of Poverty

Category: Organizations Relieving Poverty

Address: 2030 – 10013 RIVER DR

City: RICHMOND

Province, territory, outside of Canada: BC

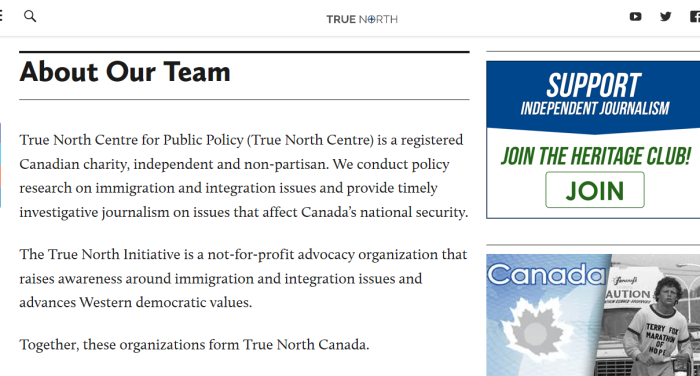

From “About Us” On Website

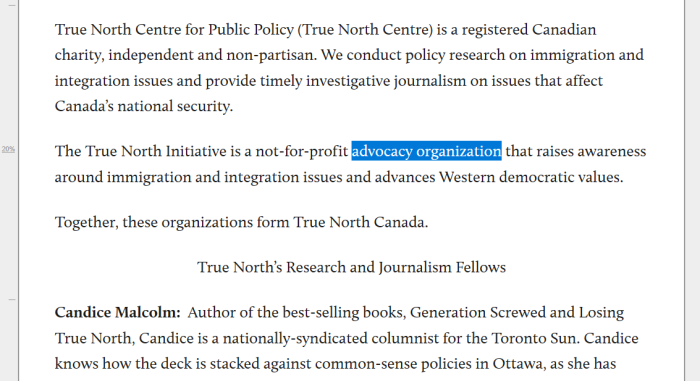

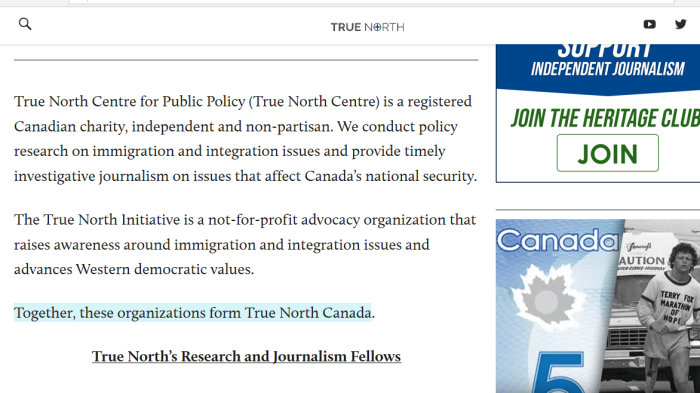

True North Centre for Public Policy (True North Centre) is a registered Canadian charity, independent and non-partisan. We conduct policy research on immigration and integration issues and provide timely investigative journalism on issues that affect Canada’s national security.

.

The True North Initiative is a not-for-profit advocacy organization that raises awareness around immigration and integration issues and advances Western democratic values.

.

Together, these organizations form True North Canada.

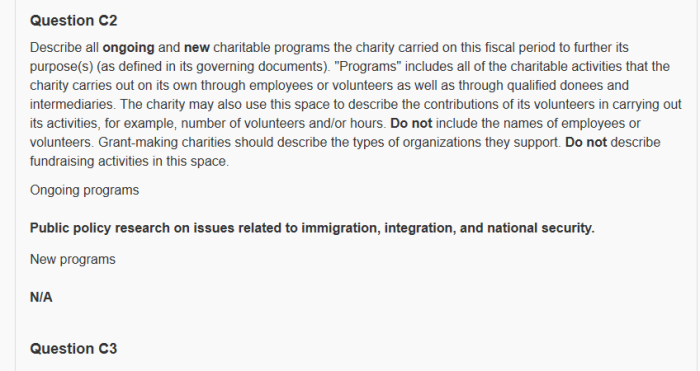

Interesting. On its own website, True North Canada claims to be about conducting policy research on immigration and integration issues.

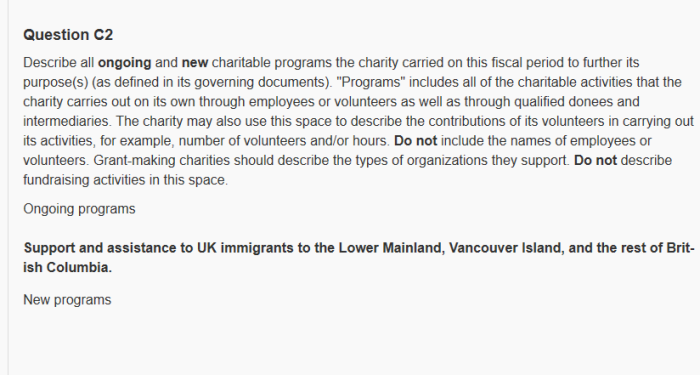

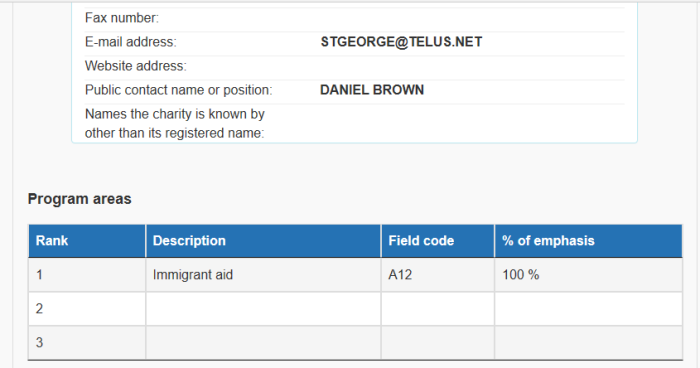

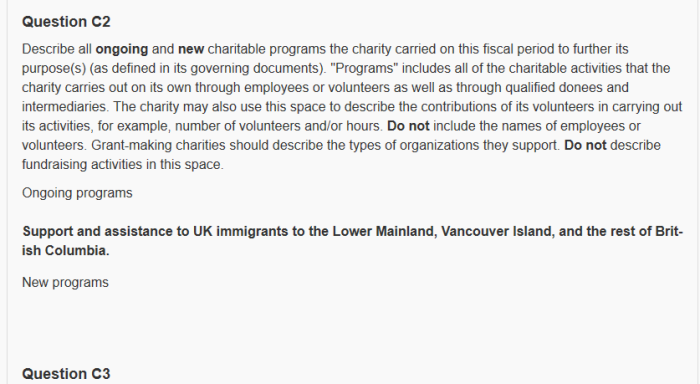

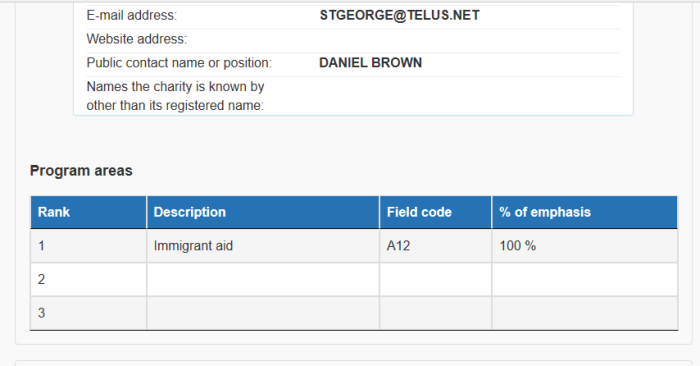

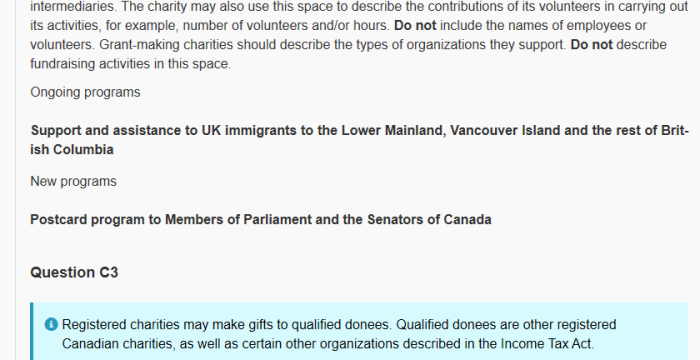

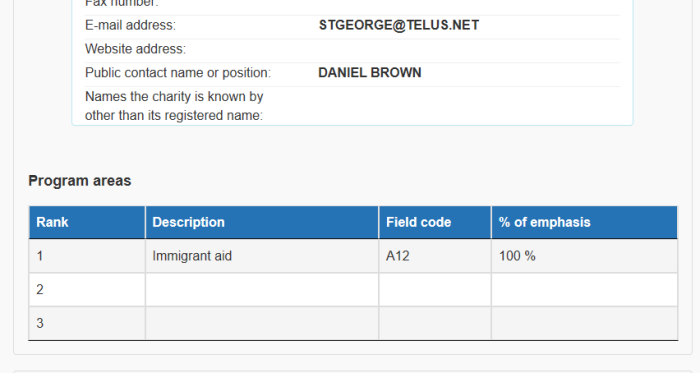

However, in tax filings True North Centre for Public Policy (which claims to be a charity) says the organization is about relieving poverty. It also claims to be helping UK immigrants settle into BC.

The reason for this discrepancy is that the Independent Immigration Aid Association (I.I.A.A.) that was founded in 1994 was taken over by Candice Malcolm. It was renamed as TRUE NORTH CENTRE FOR PUBLIC POLICY. An interesting point to raise: why take it over? Why not just start a brand new organization?

It could be to continue the tax benefits that come with being a registered charity, which True North Center still officially is.

5. Registered Charity Information Returns, 2014

Director/trustee and like official # 1

Full name: Daniel J Brown

Term Start date: 2014-01-01

Term End date: 2014-12-31

Position: President

At Arms Length with other Directors? Yes

Director/trustee and like official # 2

Full name: Roger A Dawson

Term Start date: 2014-01-01

Term End date: 2014-12-31

Position: Vice President

At Arms Length with other Directors? No

Director/trustee and like official # 3

Full name: Carole Clark

Term Start date: 2014-01-01

Term End date: 2014-12-31

Position:

At Arms Length with other Directors? No

Director/trustee and like official # 4

Full name: Robert Davies

Term Start date: 2014-01-01

Term End date: 2014-12-31

Position:

At Arms Length with other Directors? Yes

Director/trustee and like official # 5

Full name: Thomas Viccars

Term Start date: 2014-05-01

Term End date: 2014-12-31

Position:

At Arms Length with other Directors? Yes

Director/trustee and like official # 6

Full name: Tom Moses

Term Start date: 2014-05-01

Term End date: 2014-12-31

Position:

At Arms Length with other Directors? Yes

Director/trustee and like official # 7

Full name: Peter Howard

Term Start date: 2014-01-01

Term End date: 2014-12-31

Position:

At Arms Length with other Directors? Yes

6. Registered Charity Information Returns, 2015

Director/trustee and like official # 1

Full name: Daniel J Brown

Term Start date: 2015-01-01

Term End date: 2015-12-31

Position: President

At Arms Length with other Directors? Yes

Director/trustee and like official # 2

Full name: Roger A Dawson

Term Start date: 2015-01-01

Term End date: 2015-12-31

Position: Vice President

At Arms Length with other Directors? No

Director/trustee and like official # 3

Full name: Carole Clark

Term Start date: 2015-01-01

Term End date: 2015-12-31

Position: At Large

At Arms Length with other Directors? No

Director/trustee and like official # 4

Full name: Robert Davies

Term Start date: 2015-01-01

Term End date: 2015-12-31

Position: At Large

At Arms Length with other Directors? Yes

Director/trustee and like official # 5

Full name: Thomas Viccars

Term Start date: 2015-01-01

Term End date: 2015-12-31

Position: At Large

At Arms Length with other Directors? Yes

Director/trustee and like official # 6

Full name: Tom Moses

Term Start date: 2015-01-01

Term End date: 2015-12-31

Position: At Large

At Arms Length with other Directors? Yes

Director/trustee and like official # 7

Full name: Peter Howard

Term Start date: 2015-01-01

Term End date: 2015-12-31

Position: At Large

At Arms Length with other Directors? Yes

7. Registered Charity Information Returns, 2016

Director/trustee and like official # 1

Full name: Daniel J Brown

Term Start date: 2016-01-01

Term End date: 2016-12-31

Position: President

At Arms Length with other Directors? Yes

Director/trustee and like official # 2

Full name: Roger A Dawson

Term Start date: 2016-01-01

Term End date: 2016-12-31

Position: Vice President

At Arms Length with other Directors? No

Director/trustee and like official # 3

Full name: Carole Clark

Term Start date: 2016-01-01

Term End date: 2016-12-31

Position: At Large

At Arms Length with other Directors? No

Director/trustee and like official # 4

Full name: Robert Davies

Term Start date: 2016-01-01

Term End date: 2016-12-31

Position: At Large

At Arms Length with other Directors? Yes

Director/trustee and like official # 5

Full name: Tom Moses

Term Start date: 2016-01-01

Term End date: 2016-12-31

Position: At Large

At Arms Length with other Directors? Yes

Director/trustee and like official # 6

Full name: Patricia Morris

Term Start date: 2016-01-01

Term End date: 2016-12-31

Position: At Large

At Arms Length with other Directors? Yes

8. Registered Charity Information Returns, 2017

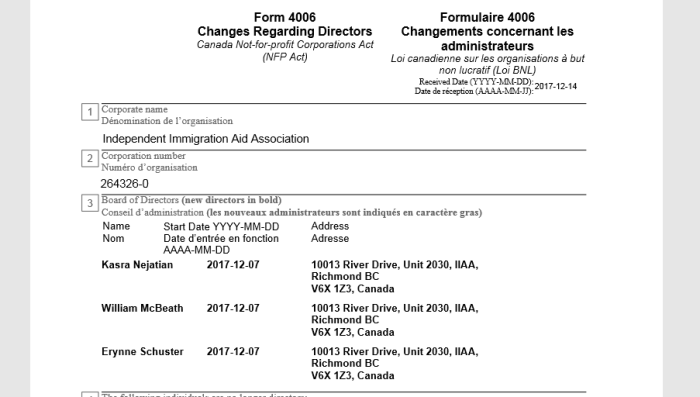

Director/trustee and like official # 1

Full name: Kasra Nejatian

Term Start date: 2017-12-07

Term End date:

Position: Director

At Arms Length with other Directors? Yes

Director/trustee and like official # 2

Full name: Erynne Schuster

Term Start date: 2017-02-07

Term End date:

Position: Director

At Arms Length with other Directors? Yes

Director/trustee and like official # 3

Full name: William McBeath

Term Start date: 2017-12-07

Term End date:

Position: Director

At Arms Length with other Directors? Yes

9. Registered Charity Information Returns, 2018

Director/trustee and like official # 1

Full name: Kasra Nejatian

Term Start date: 2017-12-07

Term End date:

Position: Director

At Arms Length with other Directors? Yes

Director/trustee and like official # 2

Full name: Erynne Schuster

Term Start date: 2017-12-07

Term End date:

Position: Director

At Arms Length with other Directors? Yes

Director/trustee and like official # 3

Full name: William McBeath

Term Start date: 2017-12-07

Term End date:

Position: Director

At Arms Length with other Directors? Yes

10. Koch/Atlas Network, Canadian Partners

- Alberta Institute

- Canadian Constitution Foundation

- Canadian Taxpayers Federation

- Canadians For Democracy And Transparency

- Fraser Institute

- Frontier Center For Public Policy

- Institute For Liberal Studies

- Justice Center For Constitutional Freedoms

- MacDonald-Laurier Institute For Public Policy

- Manning Center

- Montreal Economic Institute

- World Taxpayers Federation

These “think tanks” all promote the same things: economic libertarianism; mass economic immigration; liberal or free trade; less government; larger role for private sector. Now, let’s connect some dots.

Spoiler alert: you will notice that none of the connections you are about to be shown actually appear in True North Canada’s public information. Almost like they didn’t want the public to know.

11. Candice Malcolm’s Ties To Koch/Atlas

Candice worked for Koch and the Fraser Institute, before getting into journalism. She now runs True North Initiative, which “identifies” as a non-profit group. Of course, there is also True North Center, which “identifies” as a charity.

This was a November 2014 Atlas gettogether to complete “THINK TANK LEADERSHIP TRAINING”, whatever that means. Canadian Taxpayer’s Federation rep, Candice Malcolm was there.

At this 2014 dinner, Malcolm was a member of the Canadian Taxpayer’s Federation. Yes, one of Atlas’ Canadian partners.

Malcolm leaves out any trace of her Atlas past in the TNC website. Not very candid, is it? Malcolm also omits being a political staffer, for Jason Kenney, who “enriched” the GTA as Immigration Minister, and who wants to enrich Rural Alberta now.

12. Kasra Nejatian’s Ties To Koch/Atlas

Interesting side note: Kasra Nejatian (a.k.a. Kasra Levinson) is Candice Malcolm’s husband. He is a Director at the Canadian Constitution Foundation, which is also part of Atlas Network. He’s part of the CCF, and she was part of Fraser and Koch Institute.

Interesting omission on the TNC site: not only does Candice not mention that Kasra — her husband — is a Director of a Koch group (CCF), she omits that he is a Director at True North Center, the “charity” branch of True North Canada.

There’s no information about this on the website. In fact, one would have to search Revenue Canada’s records in order to find this out. The TNC site doesn’t even say that THERE ARE any Directors.

Worth pointing out, Nejatian was also a staffer, for Jason Kenney, former Federal Immigration Minister, and current Alberta Premier.

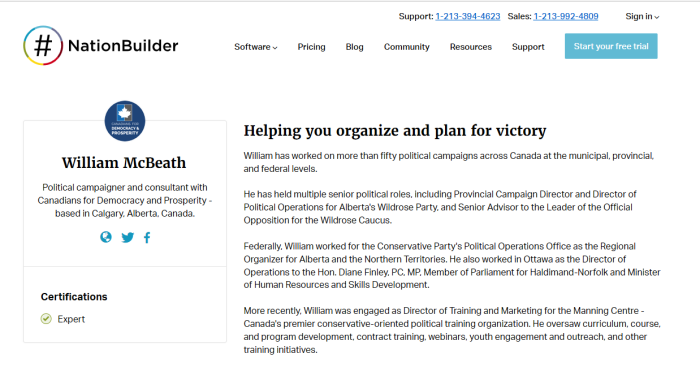

13. William McBeath’s Ties To Koch/Atlas

One of the Directors for True North’s “charity” wing is William McBeath, who used to work for the Manning Center. Again, one would have to look at the Revenue Canada website to get this information, as it is not available on TNC.news.

Interestingly, he has also held party roles with both the Alberta and Federal Conservatives. Again, no mention of this on the TNC.news website. You need to check outside information.

14. Andrew Lawton, Ontario PC Candidate

True North admits that one of their fellows, Andrew Lawton, was a candidate in the 2018 Ontario Provincial election for the Progressive Conservative Party. A refreshing bit of candour considering what they leave out.

Nothing inherently wrong with journalists getting into politics, or politicians getting into journalism. However, being so recent, it should be noted the biases and beliefs Lawton will bring to the role.

15. Charity V.S. Non-Profit: CRA

CHARITY

NON-PROFIT ORGANIZATION

Purposes

must be established and operate exclusively for charitable purposes

can operate for social welfare, civic improvement, pleasure, sport, recreation, or any other purpose except profit

cannot operate exclusively for charitable purposes

Registration

must apply to the CRA and be approved for registration as a charity

does not have to go through a registration process for income tax purposes

Charitable registration number

is issued a charitable registration number once approved by the CRA

is not issued a charitable registration number

Tax receipts

can issue official donation receipts for income tax purposes

cannot issue official donation receipts for income tax purposes

Spending requirement (disbursement quota)

must spend a minimum amount on its own charitable activities or as gifts to qualified donees

does not have a spending requirement

Designation

is designated by the CRA as a charitable organization, a public foundation, or a private foundation

does not receive a designation

Returns

must file an annual information return (Form T3010) within six months of its fiscal year-end

may have to file a T2 return (if incorporated) or an information return (Form T1044) or both within six months of its fiscal year-end

Personal benefits to members

cannot use its income to personally benefit its members

cannot use its income to personally benefit its members

Tax exempt status

is exempt from paying income tax

is generally exempt from paying income tax

may have to pay tax on property income or on capital gains

GST/HST

generally must pay GST/HST on purchases

may claim a partial rebate of GST/HST paid on eligible purchases

most supplies made by charities are exempt

calculates net tax using the net tax calculation for charities

must pay GST/HST on purchases

may claim a partial rebate of GST/HST paid on eligible purchases only if it receives significant government funding

few supplies made by NPOs are exempt

calculates net tax the regular way

Given how Revenue Canada distinguishes between charities and non-profits, this may be why Candice Malcolm took over Independent Immigration Aid Association and renamed it to True North Center for Public Policy. They likely wouldn’t be able to obtain charity status on their own. Therefore, taking an existing charity might have been an easier bet.

While True North does do decent work, there is nothing to indicate that it deserves special status, or should be registered as a charity. Otherwise, virtually any media would qualify.

Seriously, what else is the reason for acquiring the Independent Immigration Aid Association? It’s not like Malcolm, Nejatian, or any of the others wish to preserve their legacy. In fact, without looking any deeper into the topic, one would never know about it.

So did Malcolm found True North Initiative? In a deceptively technical sense, yes. The “non-profit” branch of True North Canada came from her. However, the “charity” portion which makes the organization eligible for tax perks was founded in 1994 by a completely different group of people. A lie of omission.

16. What Exactly Is True North Canada?

Press Progress picked up on the inconsistencies in Malcolm’s ever-changing description of True North Canada. So let’s go through some of them.

True North is simultaneously a media company, an advocacy group, a registered charity, and “it’s complicated“.

Could be that Malcolm wants to keep the tax breaks that come with the current structure. That could be why she “founded” True North Initiative (a non-profit), yet the True North Center for Public Policy (a charity) was a rebranded one from 1994.

Now, for a semi-related, but interesting ruling from the Federal Court of Canada.

17. Federal Court Ruling: T-1633-19

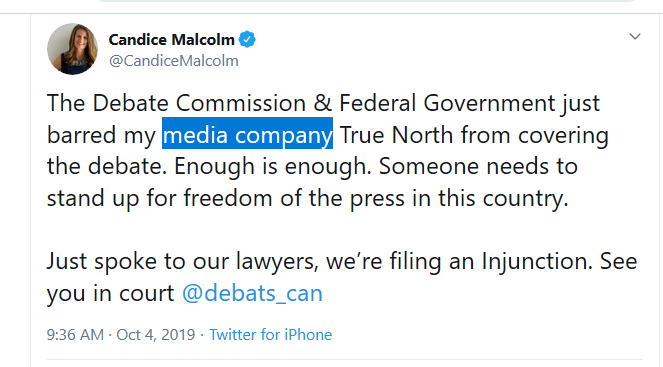

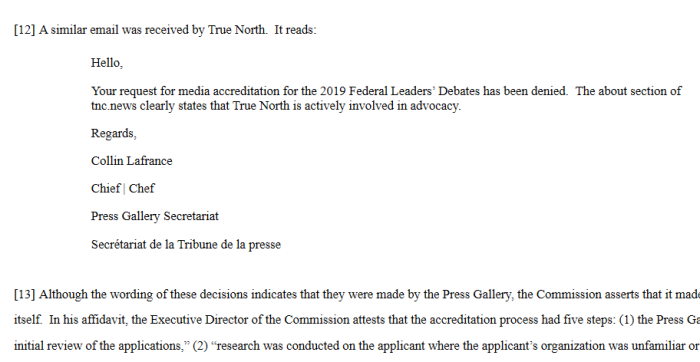

Recently, True North and Rebel Media won court cases which overturned (on an interlocutory basis) the decisions of the Elections Commissioner to restrict them from covering Federal debates in the 2019 election. This is an interesting side note to the story.

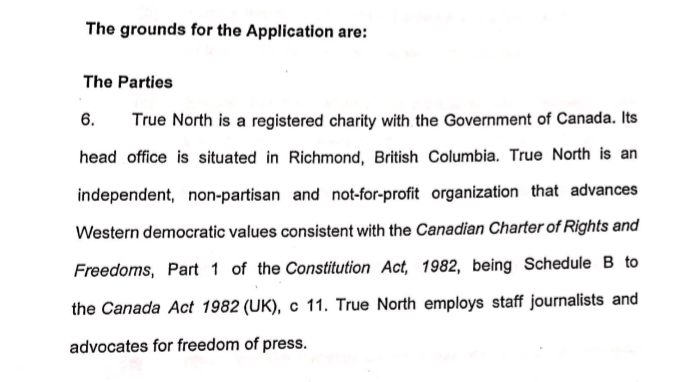

Worth stating at the front: although there were a few different names to choose from, Malcolm et al chose to use True North Center for Public Policy (the charity), for the court case.

Well, yes. They do engage in advocacy. It says so right on their website. While this may come across as pedantic, they are not wrong about this. However, things are not that simple.

The Test for the Requested Relief

[24] The test the Court must apply when asked to issue a mandatory interlocutory injunction is set out by the Supreme Court of Canada in R v Canadian Broadcasting Corp, 2018 SCC 5 [CBC] at para 18:

In sum, to obtain a mandatory interlocutory injunction, an applicant must meet a modified RJR — MacDonald test, which proceeds as follows:

(1) The applicant must demonstrate a strong prima facie case that it will succeed at trial. This entails showing a strong likelihood on the law and the evidence presented that, at trial, the applicant will be ultimately successful in proving the allegations set out in the originating notice;

(2) The applicant must demonstrate that irreparable harm will result if the relief is not granted; and

(3) The applicant must show that the balance of convenience favours granting the injunction. [emphasis in original]

[25] The Applicants bear the burden of proving to the Court on a balance of probabilities that they have met all three prongs of the tri-partite test. This Court observed in The Regents of University of California v I-Med Pharma Inc, 2016 FC 606 at para 27, aff’d 2017 FCA 8 that “[t]hese factors are interrelated and should not be assessed in isolation (Movel Restaurants Ltd v EAT at Le Marché Inc, [1994] FCJ No 1950 (Fed TD) at para 9, citing Turbo Resources Ltd v Petro Canada Inc (1989), 24 CPR (3d) 1 (FCA)).”

[26] The Order the Applicants seek is both extraordinary and discretionary. Given its discretionary nature, provided the tri-partite test has been met, the “fundamental question is whether the granting of an injunction is just and equitable in all of the circumstances of the case:” Google Inc v Equustek Solutions Inc, 2017 SCC 34 at para 25.

[37] There is also evidence in the record that some of the accredited news organizations have previously endorsed specific candidates and parties in general elections. The Commission responds that in those cases the advocacy was in editorials or produced by columnists. This begs the question as to where one draws the line as to what is and is not advocacy that disqualifies an applicant from accreditation. This goes to the lack of rationality and logic in the no-advocacy requirement.

This is a valid point. Most media outlets engage in some level of advocacy. So to disallow 1 or 2 outlets would be hypocritical.

[38] This also goes to the lack of transparency. Absent any explanation as to the meaning to be given to the term “advocacy” and given that the Commission accredited some organizations that have engaged in advocacy, I am at a loss to understand why the Commission reached the decisions it did with respect to the Applicants.

Agreed. The decisions weren’t really explained beyond the simple “you engage in advocacy”.

[39] Accordingly, I find that the Applicants are likely to succeed on the merits in setting aside the decisions as unreasonable.

The Procedural Fairness of the Process

[40] The application and scope of procedural fairness in administrative decision-making is explained by the Supreme Court of Canada in Baker v Canada (Minister of Citizenship and Immigration), [1999] 2 SCR 817 [Baker].

[41] It was noted at para 20 of Baker that “The fact that a decision is administrative and affects ‘the rights, privileges or interests of an individual’ is sufficient to trigger the application of the duty of fairness.” In the matters before this Court the interests of those whose accreditation applications were rejected are most certainly affected. This was not disputed by the Commission; rather it submitted that the Applicants were afforded a fair process in accordance with Baker.

[42] The Supreme Court of Canada observed at para 22 of Baker that “the duty of fairness is flexible and variable, and depends on an appreciation of the context and the particular statute and the rights affected.” In paras 23 to 27, it listed five factors that a court ought to consider when determining the content of the duty of fairness in a particular case. There is no suggestion that these are the only factors a court may consider:

(i) The nature of the decision being made and the process followed in making it;

(ii) The nature of the statutory scheme and the terms of the statute pursuant to which the decision-maker operates;

(iii) The importance of the decision to those affected;

(iv) The legitimate expectations of those challenging the decision regarding the procedures to be followed or the result to be reached; and

(v) The choices made by the decision-maker regarding the procedure followed.

Conclusion

[68] I have found that these Applicants have satisfied the tripartite test for the granting of the injunction requested. Moreover, and for the reasons above, I find that granting of the requested Order is just and equitable in all of the circumstances.

[69] For these Reasons, following the oral hearing on October 7, 2019, the Court issued the following two Orders:

the Leaders’ Debates Commission / Commission des Debats des Chefs is to grant David Menzies and Keenan [sic] Bexte of Rebel News the media accreditation required to permit them to attend and cover the Federal Leaders’ Debates taking place on Monday, October 7, 2019 in the English language and Thursday, October 10, 2019 in the French language;

the Leaders’ Debates Commission / Commission des Debats des Chefs is to grant Andrew James Lawton of the True North Centre for Public Policy the media accreditation required to permit him to attend and cover the Federal Leaders’ Debates taking place on Monday, October 7, 2019 in the English language and Thursday, October 10, 2019 in the French language;

[70] After issuing these Orders, the Applicants requested and were granted an opportunity to make submissions on costs. The Court was later informed that “the parties have resolved the issue of costs” and thus no further Order is required.

For all the issues a person may have with an outlet, such as Rebel Media or True North Canada, it was nice to see this decision happen. The public is best served with more media available.

Regardless of how sketchy True North is, Elections Canada acted in a very heavy-handed way. The Courtruling was a very welcome victory.

18. Malcolm Misrepresents On Twitter

Malcolm claims to be the FOUNDER of True North Canada in her Twitter biography. While this is true on a technical level, it omits that she and her husband took an existing charity, renamed and repurposed it, and now use it for tax benefits.

It’s not entirely clear what this “non-profit” of True North Initiative adds, other than perhaps some cover. Slapping that on a rebranded charity seems to be what counts as “founding” these days.

While I support the challenge in Federal Court (allowing coverage of the debates), it was in the spirit of open media. It is not in any way to be seen as an endorsement of this “organization”. It is deceitful and underhanded.

Discover more from Canuck Law

Subscribe to get the latest posts sent to your email.