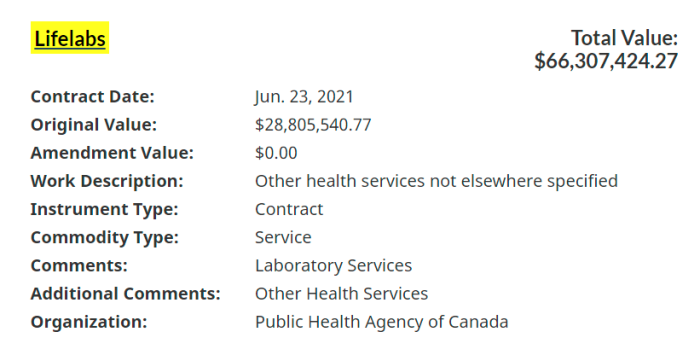

June 23, 2021, LifeLabs received a $66.3 million contract from the Public Health Agency of Canada. It was originally for $28.8 million, but the terms were amended. The company had certainly negotiated other arrangements before, but this was big. The purpose of this one was testing kits for the “virus” that’s terrorizing the world. The Minister of Public Services and Procurement would oversee the issuing of such agreements.

It’s not just the vaccine contracts that are worth a lot of money. Testing kits may in fact be worth even more, given for frequently they are used. As such, it’s important to do a little due diligence on who’s being awarded these deals.

OMERS, the Ontario Municipal Employees Retirement System, and some of its organizations have been in the spotlight before, but this most recent time needs to be discussed. It has to do with certain contracts that Ottawa had awarded. Unsurprisingly, Global News hasn’t addressed this.

The federal government has awarded three companies with contracts worth up to $631 million in total for COVID-19 border testing and other screening services.

.

Public Services and Procurement Canada says Switch Health, LifeLabs and Dynacare are carrying out testing of international travelers entering Canada at airports and land border crossings.

Last week, the Federal Government announced some $631 million to be spent for virus testing kits. Notwithstanding that the pandemic is a hoax, and the tests useless, something else is noteworthy.

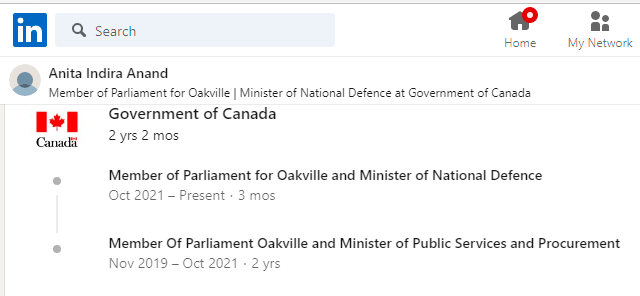

Anita Anand used to be the Minister of Public Services and Procurement. In short, it was her job to oversee large purchases made by the Canadian Government. Naturally, this requires a great deal of transparency and integrity. However, things may not be so simple.

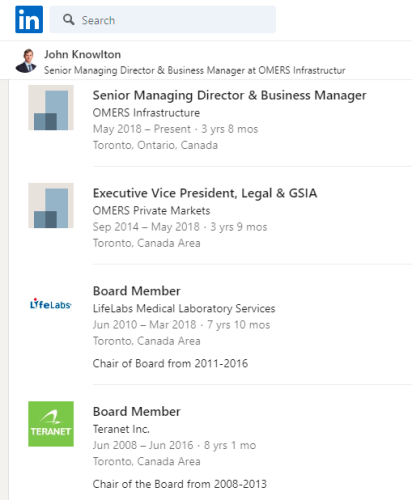

Specifically, her husband, John Knowlton, helps run OMERS. As the name implies, it manages the pension plans for many Provincial workers. Unsurprisingly, it owns stocks and bonds in other companies.

Conflicts of interest — or even the apparent conflict — must always be avoided. And this one looks far too cozy to simply be an oversight. In fairness, it could be legitimate, but does raise real questions.

Knowlton’s position is awkward, to say the least. While he’s now a Director at OMERS, he held similar roles in LifeLabs and Teranet. OMERS has interests in both of them. His company will directly profit from extra contracts awarded for testing equipment. Blacklock’s reported on this issue earlier, and it was denied that there was any insider dealing involved.

Something else happened Provincially a few months back that requires our attention. It involved engaging in some influence peddling of Doug Ford by a longtime ONPC operative.

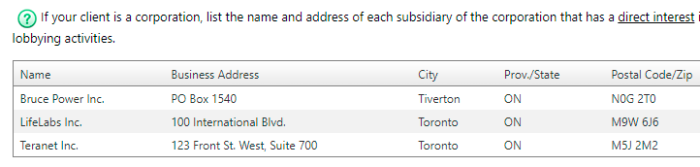

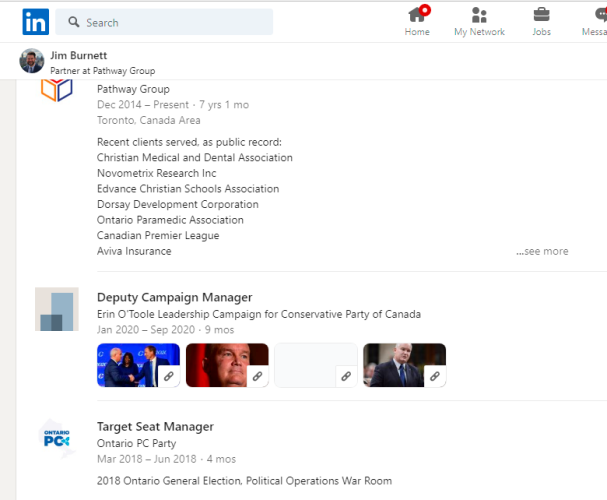

On August 5, 2021, Jim Burnett of the Pathway Group lobbied the Ontario Government on behalf of OMERS, his client. What was the nature of the lobbying? According to the Ontario Registry:

Ongoing discussions in connection with investment in LifeLabs, Teranet, and other related OMERS investments relating to diagnostic lab sector reforms and proposals for alternative service delivery models for statutory registries and associated particular government services as they arise.

In short, this meeting was about getting the Ontario Government to pump money into certain companies and by extension, OMERS. However, Burnett has quite the connected past.

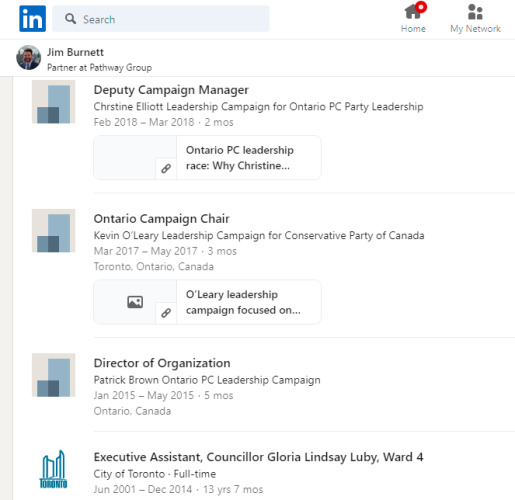

- Deputy Campaign Manager (2020, O’Toole CPC run)

- Targeted Seat Manager (ONPC, Ford 2018)

- Deputy Campaign Manager for Christine Elliott (ONPC run)

- Campaign Chair for Kevin O’Leary (2016 CPC run)

- Campaign Organizer for Patrick Brown (2015 ONPC run)

- Working for Tim Hudak (ONPC 2000 to 2001)

- Working for Ernie Hardeman (ONPC 2000)

In all honesty, this looks shady as hell. Burnett used his considerable political ties in order to advance the business interests of his new client. The fact that he was a handler for Erin O’Toole may be the reason that the CPC doesn’t seem to object to such procurement deals.

While Anita Anand seems to influence the purchasing Federally, there’s some activity going on in Ontario as well. Glad to know that everything is done above board. This happens elsewhere as well.

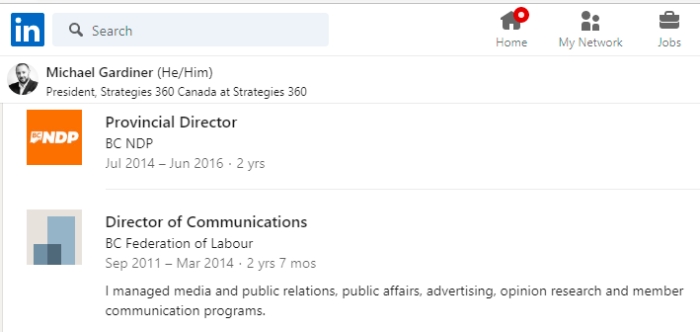

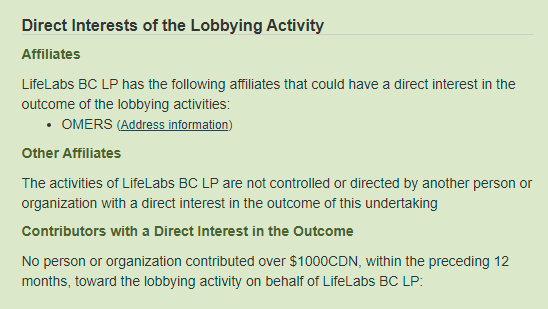

For what it’s worth, LifeLabs has been lobbying in B.C. as well, seeking more contracts. The company openly admits that OMERS may be impacted by the outcome there. The lobbyist, Michael Gardiner, is a former Provincial Director of the BCNDP. In case anyone is unaware, the NDP is currently in power in this Province.

In February 2021, Teranet paid the Saskatchewan Government a visit, to talk about purchasing a land registration system. This was done by Kory Teneycke, who currently acts as a handler for Doug Ford.

Whenever political connections are intertwined in purchases like these, it’s always beneficial to start asking questions. Now, this last subject is off topic, but needs a mention:

It’s never a good sign to be featured by the World Economic Forum. OMERS also plays along with the climate change scam. It claims that such considerations will be factored into all future decisions.

Climate change is one of the defining issues of our time. We believe that as institutional investors, we have an important role to play as the world transitions to a lower carbon economy. We are focused on growing sustainably, by developing partnerships across our portfolio and finding new investment opportunities that support the transition

OMERS has endorsed the Task Force on Climate-Related Financial Disclosures (TCFD) as it believes it is a helpful standard to deliver the information investors need to assess climate risk. We believe that engaging with our portfolio companies where climate change presents material risks, and striving to improve overall reporting and transparency, will enhance our understanding of the financial risks posed by climate change on our portfolio.

Like with other pension funds and investment companies, there appears to be a deliberate effort to embrace the green agenda laid out by Governments and their handlers. This happens even when it’s not necessarily what’s best for the plan holders.

Things are rarely as simple as they appear.

(1) https://www.blacklocks.ca/anands-husband-is-director/

(2) https://www.linkedin.com/in/anita-indira-anand-9857b229/

(3) https://globalnews.ca/news/8428125/covid-border-testing-rules-canada/

(4) https://www.linkedin.com/in/john-knowlton-aa0a55153/

(5) John Knowlton LinkedIn Profile

(6) https://www.linkedin.com/in/blake-hutcheson-55403218b/

(7) https://www.linkedin.com/company/borealis-infrastructure/

(8) https://www.omersinfrastructure.com/investments

(9) Knowlton OMERS Infrastructure – Investments

(10) https://www.omersinfrastructure.com/sustainable-investing

(11) https://www.weforum.org/organizations/omers

(12) Knowlton OMERS _ World Economic Forum

(13) https://www.sec.gov/comments/s7-05-18/s70518-3647325-162406.pdf

(14) https://lobbycanada.gc.ca/app/secure/ocl/lrs/do/advSrch

(15) https://lobbycanada.gc.ca/app/secure/ocl/lrs/do/vwRg?cno=16669®Id=911599

(16) https://lobbyist.oico.on.ca/Pages/Public/PublicSearch/SearchResults.aspx

(17) https://www.linkedin.com/in/jim-burnett-583a436b/

(18) Jim Burnett LinkedIn Profile

(19) https://www.linkedin.com/in/michael-gardiner-3b11726/

(20) Michael Gardiner LinkedIn Profile

(21) https://www.sasklobbyistregistry.ca/search-the-registry/registration-details/?id=18429fcc