The Canadian Pension Plan Investment Board is responsible for investing the money that gets taken from workers’ pay cheques. Now, what does this group actually invest in? The answers may be surprising, as it speaks to the direction they plan to take the fund.

| COMPANY | AMOUNT |

|---|---|

| 3M Co. | $51,203,000 |

| Acceleron Pharma Inc. | $85,000 |

| Agios Pharmaceuticals Inc. | $1,017,000 |

| Alexion Pharmaceuticals | $33,800,000 |

| Alnylam Pharmaceuticals | $1,329,000 |

| Amicus Therapeutics | $31,186,000 |

| Arrowhead Pharmaceuticals | $69,000 |

| Biogen | $3,749,000 |

| Biohaven Pharmaceuticals | $31,000 |

| China Biologic Products | $242,000 |

| CVS Health Corp. | $104,361,000 |

| Cardiovascular Sys Inc. | $1,339,000 |

| Checkmate Pharmaceuticals | $219,000 |

| Eli Lilly & Co. | $134,902,000 |

| Fusion Pharmaceuticals | $36,624,000 |

| GW Pharmaceuticals | $173,115,000 |

| Gilead Sciences | $85,944,000 |

| HCA Healthcare | $20,325,000 |

| Healthpeak Properties Inc. | $43,159,000 |

| Horizon Therapeutics | $688,000 |

| Hutchison China Meditech | $3,145,000 |

| Ionis Pharmaceuticals | $2,414,000 |

| Johnson & Johnson | $479,225,000 |

| Ligand Pharmaceuticals | $466,000 |

| Magellan Health | $5,683,000 |

| Medifast Inc. | $641,000 |

| Medpace Holdings Inc. | $15,813,000 |

| Merck & Co. | $379,344,000 |

| Mirati Therapeutics | $61,000 |

| Moderna | $75,193,000 |

| Neurocrine Biosciences | $752,000 |

| Novavax Inc. | $56,000 |

| Opko Health Inc. | (Sold off) |

| Orthofix Med Inc. | $976,000 |

| PTC Therapeutics | $13,561,000 |

| Pacira Biosciences | $13,925,000 |

| Pfizer Inc. | $224,969,000 |

| Phillip Morris | $128,347,000 |

| Physicians Realty Trust | $5,618,000 |

| Prestige Consumer Healthcare | $1,022,000 |

| Procter & Gamble | $498,019,000 |

| Quest Diagnostics | $130,317,000 |

| Reata Pharmaceuticals | $323,000 |

| Regeneron Pharmaceuticals | $3,233,000 |

| Royalty Pharma | $5,420,000 |

| Sabra Healthcare REIT | $6,232,000 |

| Sage Therapeutics | $735,000 |

| Sigilon Therapeutics | $71,333,000 |

| Starr Surgical Co. | $21,247,000 |

| Teladoc Health Inc. | $4,796,000 |

| Tenet Healthcare Corp. | $14,267,000 |

| Teva Pharmaceuticals | $1,723,000 |

| Theravance Biopharma | $169,000 |

| Thermo Fisher Scientific | $198,939,000 |

| Trevi Therapeutics | $36,000 |

| Trillium Therapeutics | $1,431,000 |

| Ultragenyx Pharmaceutical | $1,000 |

| United Therapeutics Corp. | $413,000 |

| Unitedhealth Group Inc. | $1,067,720,000 |

| Usans Health Sciences | $5,867,000 |

| Viatris Inc. | $16,153,000 |

| West Pharmaceutical SVSC | $410,000 |

| Zimmer Biomet | $19,398 |

Aside from all of the stocks in pharmaceuticals and health care, the CPPIB has interests in many other organizations that will raise eyebrows. True, the “Great Reset” may be a massive conspiracy theory, but the investments here would suggest otherwise.

| COMPANY | AMOUNT |

|---|---|

| Alphabet Inc. | $2,188,964,000 |

| Amazon Inc. | $779,986 |

| American Express | $134,979,000 |

| Apple Inc. | $979,811,000 |

| Aramark | $19,240,000 |

| Autodesk | $19,044,000 |

| Bank of America | $372,509 |

| Bank of Montreal | $62,350 |

| Bank of Nova Scotia | $216,553,000 |

| Best Buy | $12,943,000 |

| Blackline Inc. | $493,000 |

| Blackrock | $230,895,000 |

| Blackstone | $53,059,000 |

| Boeing | $70,565,000 |

| Citigroup | $319,809,000 |

| Comcast Corp. | $65,150,000 |

| E-Bay | $15,259,000 |

| Equifax | $135,602,000 |

| Fox Corp. | $4,632,000 |

| Hewlett Packard | $121,000 |

| Home Depot | $274,181,000 |

| Icici Bank Limited | $59,222,000 |

| JP Morgan Chase | $876,096,000 |

| Mastercard Incorporated | $2,236,387,000 |

| Microsoft Corp | $1,143,414,000 |

| Molson Coors Beverage | $8,593,000 |

| NASDAQ | $5,116,000 |

| Newscorp | $470,000 |

| Paycom Software | $993,000 |

| Paychex Inc. | $19,982,000 |

| PayPal Holdings | $228,341,000 |

| $611,000 | |

| Rogers Communications | $1,500,000,000 |

| Royal Bank of Canada | $537,548,000 |

| Shaw Communications Inc. | $100,269,000 |

| Shopify | $244,903,000 |

| Starbucks Corp. | $32,580,000 |

| Synchrony Financial | $5,553,000 |

| Target Corp. | $29,903,000 |

| Tesla Inc. | $128,538,000 |

| Toronto Dominion Bank | $289,035,000 |

| Transunion | $37,293,000 |

| Trip Advisor | $1,468,000 |

| Twitter Inc. | $57,887,000 |

| Uber Technologies | $60,382,000 |

| Verizon Communications | $192,559,000 |

| Visa Inc. | $135,000 |

| Vonage Holdings Corp | $145,000 |

| Walmart Inc. | $245,483,000 |

| Zoom Video Communications | $5,807,000 |

For reference, Alphabet Inc. is the company that owns Google and its subsidiaries, such as YouTube. It seems that being major stakeholders in the business will have great influence over the social media censorship that Governments ask them to play. CPPIB holds over $2 billion. Difficult to say no to your biggest shareholders.

Additionally the CPPIB holds over $50 million in stock in Twitter. This platform has also been brutal when it comes to censoring views that contradict official pandemic or election narratives.

This is certainly quite in the interesting portfolio: pro-big pharma, and pro-Great Reset. However, there is a bigger and more fundamental problem that needs to be addressed: liabilities.

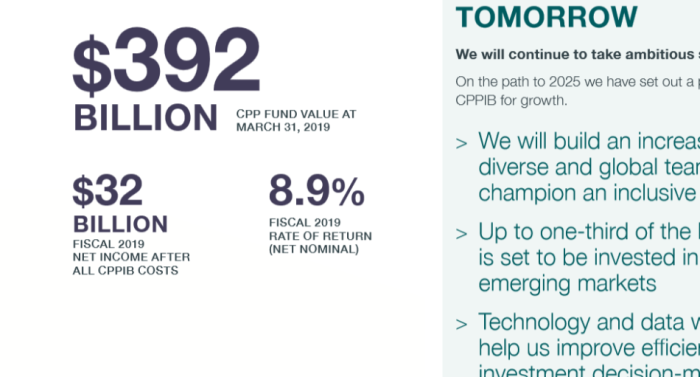

| Year | Value of Fund | Inv Income | Rate of Return |

|---|---|---|---|

| 2010 | $127.6B | $22.1B | 14.9% |

| 2011 | $148.2B | $20.6B | 11.9% |

| 2012 | $161.6B | $9.9B | 6.6% |

| 2013 | $183.3B | $16.7B | 10.1% |

| 2014 | $219.1B | $30.1B | 16.5% |

| 2015 | $264.6B | $40.6B | 18.3% |

| 2016 | $278.9B | $9.1 | 6.8% |

| 2017 | $316.7B | $33.5B | 11.8% |

| 2018 | $356.B | $36.7B | 11.6% |

| 2019 | $392B | $32B | 8.9% |

The CPPIB routinely crows about how well its investments do, and how the fund is worth hundreds of billions of dollars. The problem is that it has a screwy accounting system. Instead of taking into account all assets and liabilities, the health is determined by ability to meet current obligations. The fund has been properly accounted, and there is over $1 trillion in unfunded liabilities. This is money taken in an spent, for which it (should have been) paid out.

Most pension systems act as a ponzi scheme, where the only way to meet old obligations is with the infusion of new money. Clearly, such a system is unsustainable in the long term.

But hey, at least our investments in Pfizer, Moderna, Johnson & Johnson, Gilead, Eli Lilley and 3M are doing well. Good thing there is a “pandemic” to drive up demand for these products.

To hell with free speech and open media.

Big pharma is here to stay.

https://www.sec.gov/edgar/browse/

https://www.sec.gov/edgar/browse/?CIK=1283718

https://www.sec.gov/Archives/edgar/data/1283718/000110465921024475/xslForm13F_X01/infotable.xml

https://www.cppinvestments.com/the-fund/our-performance

https://canucklaw.ca/pensions-1b-unsustainable-underfunded-takes-money-out-of-canada/